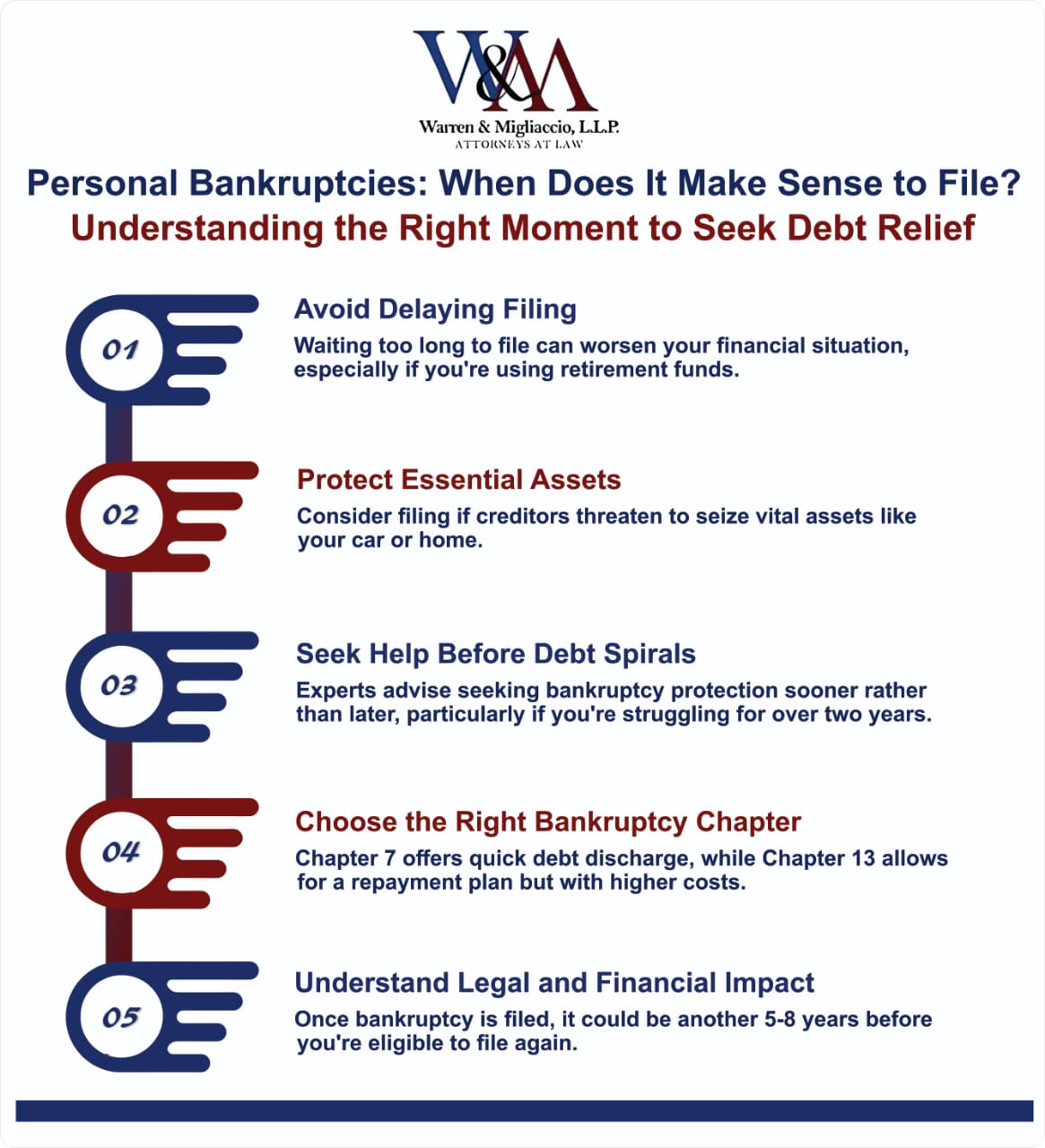

Filing for personal bankruptcies is a tough decision, but delaying it can make financial troubles worse.

Bankruptcy filings remain below pre-pandemic levels but have risen sharply in the past year. In October, personal bankruptcies increased by 16% compared to the same time last year. More Americans are turning to bankruptcy for relief. Experts urge those facing debt to consider it sooner rather than later.

Why Do People Wait to File?

“Consumers in financial distress rarely prioritize bankruptcy,” said Michael Hunter, vice president at Epiq Aacer, a partner of the American Bankruptcy Institute (ABI). Most people wait 18 to 24 months after hardship begins before filing.

Decades of research show this trend. Interviews with thousands of filers reveal that two-thirds endure financial struggles for up to five years before seeking relief.

Robert Lawless, a law professor at the University of Illinois and co-investigator for the Consumer Bankruptcy Project, confirmed this pattern. “People often wrestle with debt for over two years before considering legal options,” he told CBS MoneyWatch.

Misunderstandings About Bankruptcy

Many delay filing due to misconceptions about bankruptcy. Lawless said this often leads to worse financial strain. “Seeking help earlier can save people unnecessary hardship,” he explained. Lawless, a founding member of the Consumer Bankruptcy Project, emphasized the need for awareness about bankruptcy’s benefits.

Signs It’s Time to File

The stigma surrounding bankruptcy makes many see it as a last resort. This hesitation often leads people to use up retirement savings or other protected assets. Filing could preserve these funds.

How do you decide when it’s time to seek relief under federal bankruptcy protection? Here are five signs that bankruptcy might be a wise option.

- You’re using credit cards to make ends meet. If your debts have been building for some time and your income has remained steady, you may have found there isn’t enough cash to cover your living expenses, credit payments, and still keep food on the table. This often begins a vicious cycle when people begin using credit cards to pay bills so they have enough cash to cover the minimum payments on the credit cards. Additionally, “dipping into retirement accounts is a major warning sign,” Lawless said. These accounts are typically safe from creditors in bankruptcy. Borrowing money for daily expenses is another red flag.

- You’ve stopped planning for the future. When every cent you earn goes toward your debt, it’s hard to think about the future. You may have stopped saving for home improvements, retirement, or even for emergencies, putting all your funds toward debt reduction with no improvement in your overall financial health.

- Your credit card balances are growing even though you’re not spending. If you make only minimum payments on your credit cards, you are charged interest on the balance you carry. The interest then becomes part of the principal amount due, and you are charged interest on that as well. Add in late charges and over-the-limit fees, and the balance can easily grow in a very short period of time.

- You’re afraid to answer the phone. Creditors are relentless in their attempts to collect debt once you’ve fallen behind in your payments. If you dread the arrival of mail each day because of the stack of past due notices you know will be waiting, or don’t answer the phone to avoid harassing calls, it might be time to consider bankruptcy. Pamela Foohey, a law professor at the University of Georgia, advised filing if creditors threaten essential assets like a car or home. “Bankruptcy can protect you from wage garnishments, repossession, or losing your home,” Foohey said.

- Your health is deteriorating from chronic stress. Strong people show what they’re made of when things get tough. But ongoing financial difficulty, especially when it’s getting worse in spite of your best efforts, will eventually affect your health. Insomnia, heartburn, headaches and hypertension all are associated with stress. Deteriorating health will eventually affect your work performance, further jeopardizing your situation.

Ask Yourself These Questions

Here are a few questions you can ask yourself to indicate what your next move should be to avoid total financial disaster:

- Are you in the red each month?

- Is it almost impossible just to make the minimum monthly credit card payments?

- Have you sacrificed essential items just to have the money to pay monthly credit card payments?

- Are bill collectors calling?

- Have you eliminated all the “extras” like entertainment, clothing, etc., but still can’t make ends meet?

Answering yes to any of these questions is a good indicator that you should speak to a bankruptcy attorney about your options. An attorney can look at the specifics of your situation and help you work to reduce or eliminate the debts that weigh you down through the bankruptcy process.

You can help regain control over your life by taking an honest look at where you stand, making actionable steps to right your situation, and then setting out on a path of a healthier financial future.

Types of Bankruptcy: Chapter 7 vs. Chapter 13

Most filings fall under Chapter 7 or Chapter 13.

-

Chapter 7: Costs about $1,500 in upfront attorney fees. This process discharges debts in 3 to 6 months by selling nonexempt assets. However, 95% of cases don’t involve selling anything, according to Lawless.

-

Chapter 13: Spreads payments over 3 to 5 years and costs about $4,500 in attorney fees. These fees can be included in the repayment plan. Many choose Chapter 13 to catch up on mortgage payments.

Foohey explained that Chapter 13 can help save homes, but Lawless warned some opt for it only to afford legal fees. He suggested Congress allow Chapter 7 fees to be paid over time to avoid this problem.

Explore the best time to file for bankruptcy, how it can protect your assets, and the differences between Chapter 7 and Chapter 13 filings.

Bankruptcy Trends Post-COVID

Before COVID-19, about 750,000 people filed for bankruptcy each year. Filings dropped sharply during the pandemic due to government aid, stimulus payments, and loan forbearance.

Michael Hunter of Epiq described the drop. “Bankruptcies fell to less than half of pre-pandemic levels due to financial support programs,” he said.

As aid ended, household debt rose, but filings didn’t surge. Lawless expects filings to return gradually to pre-pandemic levels. By October 2024, nonbusiness bankruptcies reached 405,132.

“We’re still far from 2019 levels,” Foohey said. However, the trend points to a slow return to normalcy after pandemic disruptions.

[elementor-template id=”29201″]