Quick Answer

If LVNV sues you in Texas, respond fast: file your Answer on time, demand proof, review whether the claim is time-barred, and speak with counsel before the case moves forward.

-

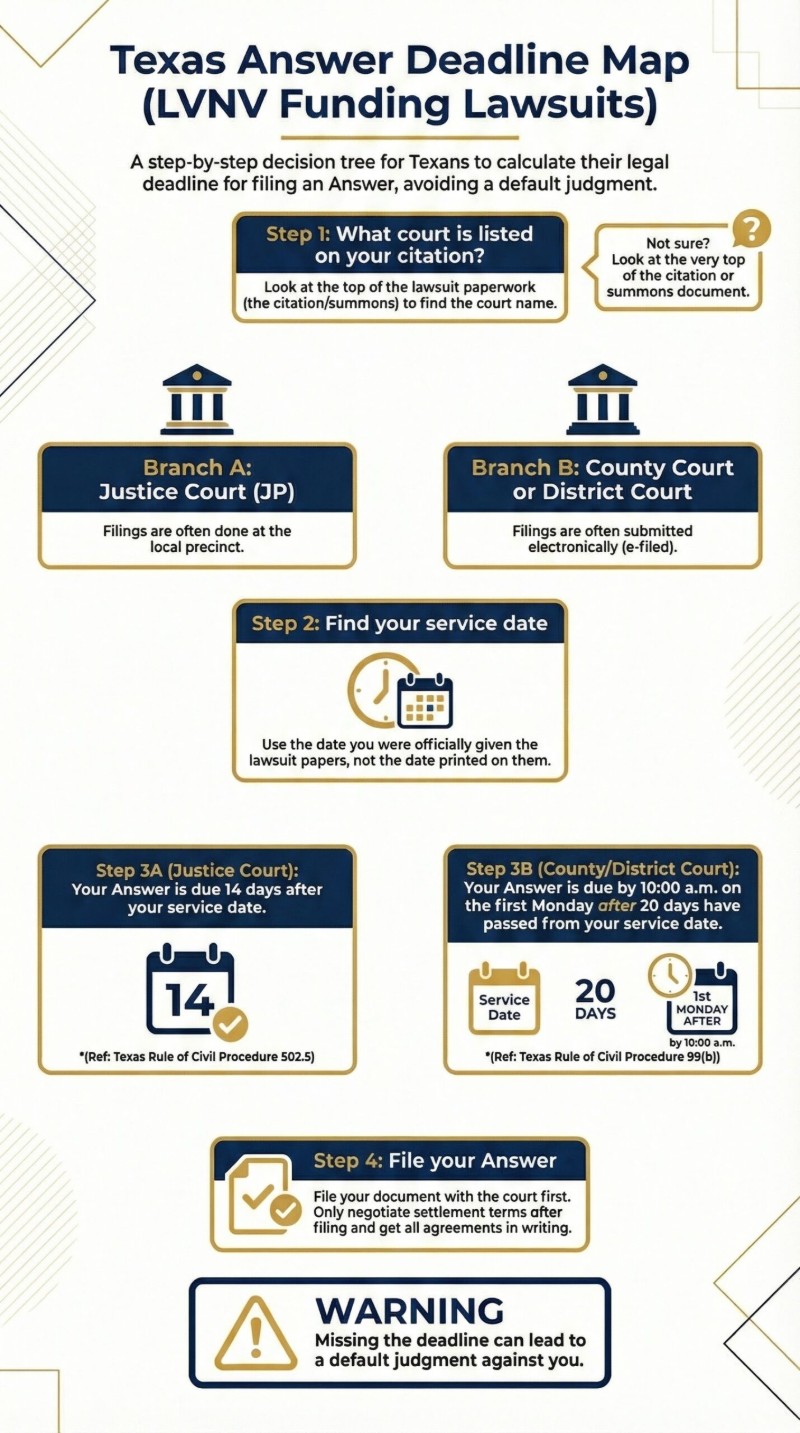

File your Answer on time: 14 days in Justice Court or by 10 a.m. on the Monday after 20 days in county or district court.

-

Demand proof of ownership and account records, and review whether Texas’s four-year statute of limitations may bar the claim.

-

Speak with a Texas debt-defense attorney about defenses, settlement options, and the next step in your case.

Hear It From the Attorney: What to Do When LVNV Funding Sues You in Texas

Attorney Christopher Migliaccio explains the deadlines, proof problems, and defenses that matter most when LVNV Funding sues you in Texas.

Press play to see captions…

| Comparison Point | Justice Court (JP) | County/District Court |

|---|---|---|

| Typical Answer deadline | 14 days after service | 20 days + next Monday at 10 a.m. |

| How to respond | File pro se or through counsel at the precinct; some allow e-file | E-file an Answer, often through counsel |

| Common LVNV proof issues | Gaps in chain of title; generic affidavits; incomplete account histories | Missing cardmember agreement; interest/fees math; hearsay in business-records affidavit |

| Court type named in article as a forum for debt-buyer cases | Yes | Yes |

These days, it is easy to get into debt. If the debt is yours and the agreement is valid, you generally owe the money, but lawsuits can still involve disputes about who owes the debt, how much is owed, or whether the claim is too old to sue on. If that debt has turned into a lawsuit from LVNV Funding, our Texas debt‑defense firm can step in between you and the collector and help you respond.

With everything going on in the world, it might be tempting to ignore debt collection notices and phone calls. But ignoring these debt collection notices is risky. Debt collectors will often take legal debt collection action and try to get a judgment against you. This judgment cannot be ignored. Instead of going silent, you can put our legal team between you and LVNV Funding and work toward a resolution that fits your situation.

The Fair Debt Collection Practices Act (FDCPA), a federal law, protects you from abusive debt collection practices. It makes sure debt collectors only try to collect legitimate debts. It also stops them from using misleading or unfair debt collection attempts. Our Texas consumer‑law team can evaluate whether LVNV’s conduct in your case violates these rules and pursue remedies if it does.

If you get collection notices from LVNV Funding, you might want to ignore them. But once the phone calls start, you will wish you hadn’t. Speaking with a debt‑defense attorney before things escalate can give you a clear game plan and peace of mind.

LVNV Funding, LLC is a junk debt buyer. This means they buy old debts or receivables that have been charged off. After buying a debt, they often aggressively pursue the person who owes it. Their collection efforts can feel overwhelming, which is why many Texans hire Warren & Migliaccio to deal with LVNV on their behalf.

If they cannot get the debt through phone calls, they may hire a local collection attorney. This attorney can file a lawsuit to recover the debt. When that lawsuit arrives, you need your own Texas debt‑defense lawyer advocating for you in the same courthouse.

If you receive notice that LVNV Funding, LLC is suing you, you should speak with a debt lawsuit defense attorney. If you live in Texas, the experienced attorney at Warren and Migliaccio can help you avoid a default judgment. Call us as soon as you are served so we can calculate your deadline and start protecting your rights.

📥 Download: Texas Answer Deadline + First 48 Hours Quick Guide (LVNV)

Save this mobile-friendly PDF so you can calculate your Answer deadline fast and follow the right steps before LVNV can push for a default judgment.

- Texas Answer deadline calculator

- First 48 hours step checklist

- LVNV proof and red flags

- Time-barred debt law snapshot

No email required. Instant PDF download.

Who is LVNV Funding LLC and why are they suing me?

If you are unfamiliar with the company’s name, you may be quite confused when you receive notice that you are being sued. Owned by Sherman Financial Group, LVNV Funding, LLC is a company that purchases debts that have been written off by original lenders. However, the account is managed by Resurgent Capital Services. This means you will likely receive letters or calls from Resurgent, not LVNV directly. If you are hearing from Resurgent, you are dealing with an LVNV account.

These debts are most often credit cards, but could also include personal loans or installment loans. There is a potential advantage with this specific debt buyer: Resurgent Capital Services typically has a policy of deleting the collection tradeline from your credit report entirely once the debt is resolved, rather than just marking it “Paid.” We can verify if your account qualifies for this deletion during settlement negotiations. Our firm regularly defends Texans in LVNV cases involving debts from creditors such as:

It is very important to file your Answer with the court listed on your citation (summons) by your deadline. In most cases, you also must send a copy of your filed Answer and other papers to LVNV’s attorney (or to LVNV if no attorney is listed). When you retain Warren & Migliaccio, our team prepares and files these responses on your behalf. Tex. R. Civ. P. 99(b); Tex. R. Civ. P. 21a; Tex. R. Civ. P. 502.5; Tex. R. Civ. P. 501.4.

After LVNV Funding buys a debt, they aggressively pursue the person who owes it with phone calls. Consumers sometimes report conduct they believe is harassing; if you experience this, keep records and speak with our firm about your options.

The Federal Trade Commission has issued rules to regulate debt collection practices. The Fair Debt Collection Practices Act (FDCPA) stops debt collectors from using false, deceptive, or misleading tactics. This law protects consumers from unfair collection efforts and opens the door for legal debt relief strategies. Our attorneys can review LVNV’s letters and calls in your case and advise whether they crossed the line.

What To Expect If You Are Contacted By Or Sued by LVNV Funding, LLC?

If LVNV Funding contacts you, the first call typically includes a debt settlement offer—often a discounted lump-sum payment if you act quickly. Before agreeing to anything on the phone, speak with a debt‑defense attorney who is looking out for you, not the collector.

If you don’t accept, they may escalate their efforts, sometimes crossing into harassment. Expect frequent calls, including to numbers of people listed as references. They also report debts to credit bureaus like TransUnion, Experian, and Equifax. Once you hire our firm, LVNV must communicate through us, which can greatly reduce the stress on you and your family.

If LVNV Funding cannot reach you or you refuse to pay, their collection activity often escalates to filing a lawsuit, seeking a judgment to recover the debt. Debt‑buyer cases may be filed in Justice Court or county/district court, depending on the amount and circumstances. Our attorneys appear regularly in both Justice Courts and county/district courts across Texas defending consumers against LVNV.

If you don’t respond or refuse to pay, they may sue you to recover the debt. LVNV Funding files thousands of lawsuits each year, often seeking more than twice the original balance. These lawsuits aim to secure default judgments when people don’t respond in time. Hiring a debt‑defense attorney early is one of the most effective ways to avoid being another default‑judgment statistic.

If LVNV is contacting you or has already sued, your next step depends on where you are right now.

Choose the situation that best matches where you are right now.

Which best describes what is happening right now?

What type of court is listed on your citation (summons)?

Do you know when you last made a payment on this debt?

Do not accept a phone offer without legal guidance

Actionable takeaway: Before agreeing to anything on the phone, speak with a debt-defense attorney who is looking out for you, not the collector. Know your income, expenses, and other debts before making an offer you can realistically afford.

Keep going: Resurgent Capital Services may delete the collection tradeline from your credit report entirely once the debt is resolved, which your attorney can verify during negotiations. Keep reading for the proof problems LVNV cases often have.

This tool gives general information only and does not create an attorney-client relationship.

If this matches where you are right now, a free consultation can help you decide how to respond.

You may have protections under federal law

Actionable takeaway: Keep records of every call, including dates, times, and what was said. The Fair Debt Collection Practices Act (FDCPA) bars debt collectors from using false, deceptive, or misleading tactics against you.

Keep going: Once you hire an attorney, LVNV must communicate through your lawyer, which can greatly reduce the stress on you and your family. Keep reading for how FDCPA violations can strengthen your defense if LVNV files a lawsuit.

This tool gives general information only and does not create an attorney-client relationship.

If this matches where you are right now, a free consultation can help you decide how to respond.

Your first move is the Justice Court Answer deadline

Actionable takeaway: File your Answer within 14 days after service and send a copy to LVNV’s attorney as required. File first, then negotiate settlement terms only after your Answer is on record.

Keep going: If you do not respond or show up in court, LVNV can get a default judgment for the full amount they asked for. Keep reading for the documentation problems and proof gaps that can help you defend or resolve the lawsuit.

This tool gives general information only and does not create an attorney-client relationship.

If this matches where you are right now, a free consultation can help you decide how to respond.

Your first move is the county or district court Answer deadline

Actionable takeaway: File your Answer by 10:00 a.m. on the first Monday after 20 days from service and send a copy to LVNV’s attorney as required before doing anything else.

Keep going: Missing that deadline can result in a default judgment, which may lead to bank-account garnishment and property liens. Keep reading for the proof problems and documentation gaps that can affect what happens next.

This tool gives general information only and does not create an attorney-client relationship.

If this matches where you are right now, a free consultation can help you decide how to respond.

Your debt may be time-barred under Texas law

Actionable takeaway: Texas has a four-year statute of limitations for most consumer debts. If LVNV is acting as a debt buyer and the limitations period has expired, Texas Finance Code §392.307 bars them from filing suit.

Keep going: A later payment or reaffirmation does not revive a time-barred claim for a debt buyer under that statute. This can be a strong defense in your Answer. Keep reading for how this defense works alongside proof-of-ownership challenges.

This tool gives general information only and does not create an attorney-client relationship.

If this matches where you are right now, a free consultation can help you decide how to respond.

Your account history holds the answer

Actionable takeaway: The statute of limitations clock in Texas depends on when the last payment or acknowledgment occurred. Check your records and gather any account statements you have.

Keep going: Bring those documents to a consultation so an attorney can assess whether the four-year time limit has passed. Keep reading to see how the statute of limitations and proof-of-ownership issues work together as defenses.

This tool gives general information only and does not create an attorney-client relationship.

If this matches where you are right now, a free consultation can help you decide how to respond.

Post-judgment deadlines can still matter

Actionable takeaway: You may be able to challenge a judgment through a post-judgment motion in the trial court (such as a motion to set aside or motion for new trial) and/or by an appeal.

Keep going: Those deadlines depend on the court and can be very short. Contact an attorney immediately so no additional deadlines pass. Keep reading so you understand the consequences of judgment and how legal representation can change your position.

This tool gives general information only and does not create an attorney-client relationship.

If this matches where you are right now, a free consultation can help you decide how to respond.

In court, debt buyers are often represented by attorneys or collectors who may lack complete documentation of your debt. This can work in your favor—if you respond. Many people feel overwhelmed or embarrassed and ignore the lawsuit, but doing so can lead to an automatic judgment against you. Our firm’s job is to force LVNV to prove every element of its case or face dismissal.

If you’re considering a settlement, know your financial limits—understand your income, expenses, and debts before making an offer you can realistically afford. An experienced debt‑defense attorney can help you evaluate offers, avoid traps in settlement language, and negotiate terms you can actually keep.

If a judgment is entered, you may be able to challenge it by a post‑judgment motion in the trial court (such as a motion to set aside or motion for new trial) and/or by an appeal. The deadlines depend on the court and can be short. Tex. R. Civ. P. 329b; Tex. R. Civ. P. 505.3; Tex. R. Civ. P. 506.1; Tex. R. App. P. 26.1.

Bottom line: If LVNV Funding sues you, don’t ignore it. Responding promptly and hiring a knowledgeable attorney can make a significant difference in your outcome. The sooner you contact Warren & Migliaccio, the more options we typically have to protect you.

Law Firms that sue and file lawsuits for LVNV:

What Not To Do

Nothing. Many of the lawsuits filed by LVNV Funding go uncontested. The debt holder, unsure of what to do, often does nothing. If you are being sued by the company and you do not respond or show up in court, LVNV Funding will get the full judgment amount they asked for. Instead of freezing, reach out to our office so we can walk you through your options.

As the defendant in a debt collection lawsuit, it is very important to know your legal rights and responsibilities when you get a summons and complaint. If you don’t respond properly, you could face serious legal consequences, including a default judgment. A consultation with a debt‑defense attorney can quickly clarify what needs to happen next.

A judgment can lead to:

- Frozen or garnished bank accounts (writ of garnishment)

- Liens on non‑exempt real property (via abstract of judgment). Tex. Prop. Code § 52.001.

- Other post‑judgment collection remedies allowed by Texas law

A judgment is a public court record. The three major credit bureaus generally do not list civil judgments as a separate item on consumer credit reports, but the underlying collection account may still appear. The court’s ruling in these matters is legally binding and enforceable.

What To Do If You Are Sued by LVNV Funding, LLC

| Decision Point | What Not To Do | What To Do |

|---|---|---|

| First response | Do nothing. | File an Answer to the lawsuit right away. |

| Court participation | Do not respond or show up in court. | Go to court and show the judge you take the matter seriously. |

| Protecting your rights | Fail to respond properly and risk serious legal consequences. | Understand the legal proceedings to protect your rights in court. |

| Getting help | Freeze instead of getting guidance. | Decide if you should hire an attorney to help with your case. |

| Likely result | LVNV Funding may get the full judgment amount they asked for. | You improve your chances of getting the case dismissed or settling the debt before trial. |

If LVNV Funding, LLC has filed a lawsuit against you, follow these important steps:

- File an Answer to the lawsuit right away. This is your first and most important step in responding to the pleadings. Our office can prepare and file your Answer for you.

- Decide if you should hire an attorney to help with your case—such as the Texas debt‑defense lawyers at Warren & Migliaccio.

Going to court shows the judge you take the matter seriously. But if you seem unprepared or confused, the judge will likely side with LVNV Funding and award them the full amount they want. Appearing with an experienced debt‑defense attorney sends a clear signal that you are prepared and defended.

You need to understand the legal proceedings to protect your rights in court. Every debt case is different, and knowing which laws apply takes experience. Some defenses are a matter of law, meaning the court will decide them without needing a full trial. We walk our clients through each step so they are never guessing about what comes next.

LVNV Funding makes a lot of money from lawsuits people don’t contest. Having a debt lawsuit attorney on your side greatly increases your chances of:

- Getting the case dismissed

- Settling the debt before going to trial court

How to Start Building Your Defense Against LVNV

Once you have avoided the biggest mistake of ignoring the lawsuit and taken the first response steps, the next question is how to challenge LVNV’s claim. This is where your dispute rights, proof demands, statute-of-limitations issues, and documentation gaps can become real defenses that may lead to dismissal, leverage in settlement, or a stronger position in court.

Your Right to Dispute or Verify the Debt

Under the Fair Debt Collection Practices Act (FDCPA), you have 30 days after you receive the required written validation notice, which tells you the amount claimed and your dispute rights, to dispute the debt. If you dispute in writing within that 30‑day window, the debt collector must pause collection until it mails you verification of the debt and, if you request it in writing, the name and address of the original creditor. Our firm can prepare and send dispute and validation letters for you so you do not have to handle this alone. 15 U.S.C. § 1692g(a)–(b).

FDCPA Dispute Timeline: Your 30-Day Window

First contact from LVNV or Resurgent. The collector’s initial communication triggers a 5-day deadline to send you a written validation notice.

Validation notice must arrive. This written notice states the amount claimed, the creditor’s name, and your right to dispute. (Unless this information was in the first communication.)

Dispute in writing within 30 days of receiving the notice. If you dispute, the collector must stop all collection activity until it mails you verification of the debt.

Collection pauses. The collector cannot resume until it provides written verification. If they cannot verify, this gap can strengthen your defense in court.

15 U.S.C. § 1692g(a)–(b)

Under the FDCPA, a debt collector must send a written validation notice within five days after its initial communication (unless the required information was in the first message or you already paid). If you dispute in writing within 30 days after you receive that notice, the collector must stop collection until it mails verification of the debt. Bring any letters or notices you received from LVNV Funding to your consultation so we can review them together. 15 U.S.C. § 1692g(a)–(b).

Requesting verification helps you confirm that LVNV Funding, LLC really owns your debt. It also helps you check if the debt amount is correct. If they cannot provide the needed documents, this can strengthen your defense in state court. It may even lead to the lawsuit being dismissed. Our attorneys routinely use these documentation gaps to attack LVNV’s claims.

Always keep copies of any letters you send to dispute the debt. Also, keep any responses you get from the collector. If the collector fails to provide proper verification, you may have more defenses under federal or Texas consumer protection laws. Having an attorney review this paper trail can reveal defenses you might otherwise miss.

Texas Fin. Code §392.307(c)–(d): Debt Buyers Cannot Sue on Time-Barred Debts

Effective Sept. 1, 2019, Texas Finance Code §392.307 bars a debt buyer from filing suit or initiating arbitration to collect a consumer debt after the statute of limitations has expired (often four years for credit-card debt under Tex. Civ. Prac. & Rem. Code § 16.004). Subsection (d) also provides that a later payment or reaffirmation does not revive a time-barred claim for a debt buyer.

If you think your LVNV lawsuit may be time-barred, our office can review your account history and raise this defense for you.

Read Texas Finance Code §392.307 | Read Tex. Civ. Prac. & Rem. Code §16.004

Weaknesses of Debt Collection Lawsuits

When collection agencies like LVNV Funding file a debt collection lawsuit, they face some challenges. These weaknesses can work in your favor. Our attorneys focus on spotting and leveraging these weaknesses to defend you.

For example, in both state and federal court, the debt collector must prove they have the legal right to collect the debt and follow all proper procedures. We hold LVNV to these proof requirements in every case.

Here are some common weaknesses in their cases:

-

You might not show up in court: Debt collectors often hope you will ignore the lawsuit. If you don’t appear, they can easily get a default judgment against you.

-

Old debts: Some debts LVNV buys are very old. These old debts may be too old to enforce legally because of the statute of limitations.

-

Unclear ownership: The real ownership of the debt is often unclear. The chain of custody—who actually owns the debt—can be confusing or incomplete.

-

Affidavits signed without full knowledge: When debts are bought in large groups, the person signing affidavits often does not know the details of each debt. They may sign hundreds of affidavits without direct knowledge of the individual accounts.

Case Study: How We Beat an LVNV Lawsuit

We recently worked with a person who was completely overwhelmed by a lawsuit from LVNV Funding. They were demanding thousands for an old credit card debt he barely recognized, and he was ready to just give up. Our advice was simple: “Let’s make them prove they actually own this debt.” We filed a response and formally demanded they produce the complete paper trail showing the chain of ownership from the original bank to them. You know what happened? They couldn’t. All LVNV had was a name on a giant spreadsheet, not the actual contracts for his specific account. Faced with having to produce real evidence in court, they quietly dismissed the lawsuit. He went from facing a judgment to owing nothing, all because we challenged them to prove their case. It shows that just because they sue doesn’t mean they can win. If you are facing an LVNV lawsuit, we can evaluate whether similar weaknesses exist in your case.

Debt collectors must follow strict procedures to avoid liability for wrongful collection actions. This is especially important when there is mistaken identity, meaning they are trying to collect from the wrong individual. Our firm can help you push back if LVNV is pursuing the wrong person or the wrong amount.

Our firm has successfully defended hundreds of Texans against lawsuits from debt buyers like LVNV Funding. In many situations, the case hinges on a simple but powerful legal challenge, as illustrated by the case study above.

Possible Consequences of a Lawsuit with LVNV Funding

| Outcome | What it means | Effect on you |

|---|---|---|

| Victory in Court | The court dismisses LVNV’s lawsuit. | No judgment is entered against you. |

| Defeat in Court | LVNV wins the case and gets a judgment. | You may have to pay the debt plus extra fees or interest. |

| Settlement Agreement | You and LVNV reach an agreement to resolve the lawsuit. | You agree to pay part of the debt, and the lawsuit is dropped. |

| Default Judgment | LVNV wins because you do not respond or miss a hearing. | A judgment may be entered against you, with possible bank-account garnishment and property liens. |

Ignoring a lawsuit about an outstanding debt can lead to serious problems. These include default judgments, bank‑account garnishment, property liens, and other collection activity. Our firm focuses on helping clients avoid these worst‑case outcomes.

The outcome of the lawsuit depends on the evidence both sides present. As a consumer, you have the right to make an informed decision for your best interests. You can legally question the debt’s validity and seek professional legal advice. During your consultation, we will review LVNV’s lawsuit and explain your options in plain language.

Benefits of Retaining a Debt Defense Attorney

What a Texas debt-defense attorney does for you:

-

Advise you of your rights under Texas and federal law

-

Prepare and file your Answer before your court deadline

-

Request a dismissal of the case against you

-

Investigate LVNV’s claim for proof gaps and errors

-

Take action if LVNV or Resurgent’s conduct violates the FDCPA

-

Assert defenses such as expired statute of limitations or lack of standing

-

Negotiate a settlement if appropriate for your situation

-

Advise you of all options including trial, settlement, and post-judgment remedies

Retaining a Debt Defense Attorney Can Help You

Hiring a lawyer who focuses on debt defense offers strategic advantages. At Warren & Migliaccio, this is a core part of our practice:

- Knowledge of the law: A specialized attorney understands Texas and federal debt collection laws and can pinpoint weaknesses in LVNV Funding’s claims.

- Stronger Negotiations: Collectors often agree to more favorable settlements when they see you have legal representation.

- Procedural Guidance: An attorney ensures you meet all court deadlines and comply with local rules—avoiding costly mistakes like missing an Answer deadline.

- FDCPA Enforcement: If LVNV Funding violates consumer rights or can’t verify the debt, a lawyer helps assert those defenses.

Talk to a Texas LVNV Defense Attorney Today

If LVNV Funding is suing you, the most important thing you can do is act before your deadline passes. Our attorneys at Warren & Migliaccio can review your lawsuit, explain your options, and help you decide whether to fight the case, raise defenses such as lack of proof or the statute of limitations, or pursue a reasonable settlement. We work to protect Texans from default judgments and unnecessary collection pressure. Call (888) 584-9614 today to schedule your free consultation and get clear guidance on your next step.

Frequently Asked Questions About LVNV Funding Lawsuits in Texas

Initial Steps & Consequences

What should I do if I get a lawsuit from LVNV Funding LLC?

In Texas, respond right away by filing a formal Answer before your deadline, typically 14 days in Justice Court or by 10 a.m. on the Monday after 20 days in county/district. Never ignore the lawsuit. Filing an Answer preserves defenses and helps you avoid a no-answer default judgment (a judgment entered because no Answer was filed). Tex. R. Civ. P. 502.5; Tex. R. Civ. P. 99(b).

- Review all documents carefully; note deadlines and specific claims.

- In your Answer, respond to each allegation by admitting, denying, or stating insufficient knowledge.

- File your Answer with the court listed on the citation, and send a copy to the plaintiff or its attorney. Tex. R. Civ. P. 99(b); Tex. R. Civ. P. 21a; Tex. R. Civ. P. 502.5; Tex. R. Civ. P. 501.4.

- Consider affirmative defenses such as statute of limitations or lack of standing.

- Gather documentation related to the debt, including payment records and correspondence.

- Consult a Texas debt-defense attorney at Warren & Migliaccio.

- Continue to meet all court requirements even if negotiating.

What happens if I ignore an LVNV Funding lawsuit?

Ignoring the case almost always leads to a default judgment. In Texas, wages are generally not subject to garnishment for consumer debts, but a judgment can still be enforced through bank-account garnishment, property liens, and other remedies.

- A default judgment means you lose without presenting your side.

- Judgments can include the claimed balance plus interest, court costs, and attorney’s fees.

- Judgments may result in bank-account garnishment and liens on non-exempt property.

- They can affect your credit and be difficult to undo, so respond on time.

Legal Defenses & Your Rights

What are my legal defenses against an LVNV Funding lawsuit?

Defenses can include statute of limitations, lack of standing/assignment proof, insufficient documentation, and FDCPA/TDCA violations. Texas courts also require proper proof under business-records rules. A Texas debt-defense lawyer can identify which defenses are strongest in your case.

- Statute of limitations: Texas’s period is generally four years for credit-card debts.

- Lack of standing: LVNV must prove ownership with proper documentation.

- Insufficient documentation: Missing card agreement, interest/fees math, or account history.

- Mistaken identity or identity theft.

- Improper service.

How does the statute of limitations affect my LVNV Funding debt?

In Texas, the limitations period for most consumer debts is four years (Tex. Civ. Prac. & Rem. Code §16.004). If the claim is time-barred and LVNV is acting as a debt buyer, Texas Finance Code §392.307 prohibits filing suit or compelling arbitration, and a later payment or reaffirmation does not revive the claim.

Before limitations expire, certain activity may affect the timeline. Speak with a Texas debt-defense lawyer to evaluate dates and documents.

To protect yourself:

- Check your account history to confirm your last payment/acknowledgment.

- Bring documents to a consult to assess whether the time limit has passed.

- Use limitations as a defense in your Answer where appropriate.

Settlement & Getting Help

Can I settle with LVNV Funding after being sued?

Yes. Many debt-buyer cases settle. Offers vary by facts and proof. Lump-sum proposals are often stronger than long payment plans. Our office regularly negotiates LVNV settlements for Texas consumers.

- Keep responding to the lawsuit while negotiating.

- Get any settlement in writing before paying.

- Request appropriate credit-reporting language and a filed satisfaction/dismissal.

- Consider attorney-led negotiation for better terms.

Should I get an attorney for my LVNV Funding lawsuit?

A debt-defense attorney who regularly appears in Texas courts can make a significant difference in an LVNV case. Under Texas Rules of Civil Procedure, certain affirmative defenses — such as statute of limitations and denial of execution on an assigned account — must be verified under oath (Tex. R. Civ. P. 93), and missing the deadline to raise them can waive those defenses permanently. An experienced attorney knows how and when to assert each one.

- Identifying whether LVNV’s business-records affidavit meets the requirements of Tex. R. Evid. 803(6) and 902(10), which govern how debt buyers prove account balances in Texas courts.

- Managing Answer deadlines, discovery requests, and hearing schedules so nothing is missed.

- Negotiating settlements with Resurgent Capital Services, which manages LVNV accounts, and verifying whether your account qualifies for full tradeline deletion from credit reports.

- Pushing for dismissal when LVNV cannot produce the original cardmember agreement or a complete chain-of-title from the original creditor.

At Warren & Migliaccio, our intake process starts with a free consultation where we review your citation, calculate your Answer deadline, and identify which defenses apply to your specific account. Call (888) 584-9614 or contact us online.

Where can I get help for an LVNV Funding lawsuit (free consultations & payment plans)?

Warren & Migliaccio, L.L.P. offers free consultations for LVNV Funding lawsuits filed in Dallas, Collin, Denton, and Tarrant counties and throughout the Northern District of Texas. During that meeting, a debt-defense attorney will review your citation, confirm which court your case is in, calculate your Answer deadline, and outline which defenses may apply.

Acting early matters because Texas Answer deadlines are short — 14 days in Justice Court (Tex. R. Civ. P. 502.5) and the first Monday after 20 days in county or district court (Tex. R. Civ. P. 99(b)) — and the 30-day window to dispute the debt under the FDCPA (15 U.S.C. § 1692g) runs separately. A consultation can help you protect both deadlines at once.

Your options may include:

- Filing an Answer and fighting the lawsuit on the merits.

- Negotiating a settlement, potentially with full tradeline deletion from your credit report.

- Filing a motion to dismiss if LVNV cannot prove ownership or the claim is time-barred.

Call (888) 584-9614 or contact us online to schedule your free consultation. Payment plans are available.