Being served with a lawsuit in Texas—especially for an old credit card, medical bill, or personal loan—can be overwhelming. Many people ask, “What happens if you ignore a lawsuit?” and hope it will just go away. In reality, ignoring a debt collection lawsuit in Texas almost always makes things worse. This article explains exactly what happens if you ignore a lawsuit in Texas and what to do instead.

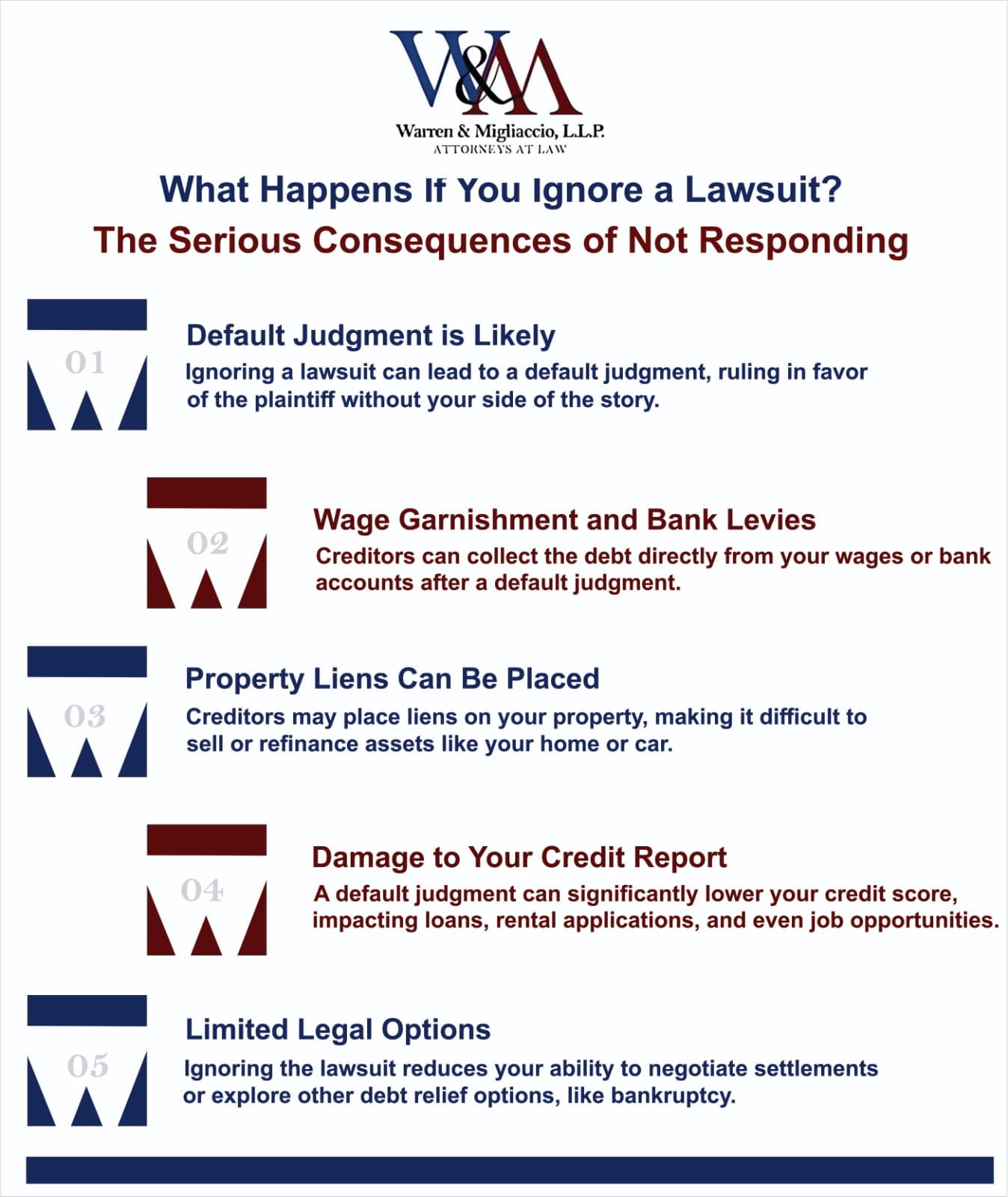

The paperwork you received (usually a citation and petition) does not mean you have to appear in court the same day, but it does start a strict countdown. Texas rules give you a limited time to file a written Answer with the court. If you miss that deadline, the plaintiff can ask the judge for a default judgment against you.

Quick answer for Texans: Under the Texas Rules of Civil Procedure, if you ignore a debt collection lawsuit and miss your Answer deadline in justice court (TRCP 502.5) or county/district court (TRCP 99(b)), the court can enter a default judgment that may follow you for years, damage your credit, and allow post‑judgment collection against your bank accounts and non‑exempt property—even though most wages for consumer debts are protected in Texas.

Quick Answer for Texans (TRCP 502.5 & 99(b))

If you ignore a Texas debt collection lawsuit, the court can treat the allegations as true and enter a default judgment once your Answer deadline passes. That judgment can last at least ten years, can often be renewed, and may allow the creditor to use post‑judgment tools like bank-account garnishment and liens on non‑exempt property.

| Texas court | Deadline to answer | Rule |

|---|---|---|

| Justice court (JP) | Generally 14 days from the date you are served | TRCP 502.5 |

| County or district court | By 10:00 a.m. on the Monday next after 20 days from service | TRCP 99(b) |

- Judgment lifespan: A Texas judgment usually lasts at least 10 years and can often be renewed for additional 10‑year periods.

- Garnishment: For most consumer debts, Texas protects your wages from garnishment, but creditors may still pursue post‑judgment bank-account garnishment and liens on non‑exempt property through separate court proceedings (see Texas Civil Practice & Remedies Code ch. 63).

- If you cannot pay: You still need to answer the lawsuit. You may have defenses, be able to negotiate a realistic settlement, or explore bankruptcy or other options with a Texas lawyer.

Served with a lawsuit? Do not ignore it. Call (888) 584-9614 or request a free consultation online before your Answer deadline.

If you are only receiving calls, letters, or texts from debt collectors and have not yet been served with a lawsuit in Texas, start with our guide on why you should not ignore debt collectors.

The Price of Silence: Understanding Default Judgments in Texas

In Texas, ignoring a lawsuit is a critical misstep that can trigger what’s called a default judgment. If someone is suing you over a consumer debt and you do not file a timely Answer with the court, the plaintiff can ask the judge to rule in their favor simply because you did not respond. In justice courts, that deadline is generally 14 days from service, and in county or district courts you generally must answer by 10:00 a.m. on the Monday next after 20 days from the date of service (learn more about what courts handle debt collection cases in Texas).

This is true whether your lawsuit is a smaller claim in justice court or a higher‑dollar case in county or district court. If you fail to file an Answer (your formal written response), the judge can rule in favor of the plaintiff without ever hearing your side. It is like forfeiting a game you might have been able to win.

Unpacking the Default Judgment Process in Texas

Here is how a default judgment usually plays out in a Texas debt collection lawsuit:

- The plaintiff (creditor or debt buyer) files a lawsuit and has you legally served with the citation and petition.

- You have a limited time to file an Answer with the court—typically 14 days in justice court or by 10:00 a.m. on the Monday next after 20 days in county or district court, depending on where the lawsuit was filed.

- If you do not file an Answer by the deadline, the plaintiff can file a Motion for Default Judgment asking the court for an automatic win.

- The court reviews the file and, if it sees that you were properly served and did not respond, will usually grant the default judgment.

- The court enters a judgment in favor of the plaintiff. At that point, you lose the chance to present defenses or challenge the amount, and the creditor can pursue post‑judgment collection.

What Happens If You Ignore a Lawsuit in Texas?

Ignoring a debt collection lawsuit in Texas sets off a chain reaction. Once a default judgment is entered, the creditor has much stronger tools to collect than it did before filing suit. You also lose valuable rights and defenses that may have helped you reduce, defeat, or resolve the claim.

Here are some of the biggest risks of ignoring a Texas lawsuit:

- You waive the chance to dispute the debt if, for example, the debt is not yours, the balance is wrong, the plaintiff cannot prove it owns the account, or the debt is past the statute of limitations.

- You lose the right to present your side of the story, raise defenses, file counterclaims, or challenge inaccurate fees, interest, or attorney’s fees.

- You make it easier for the creditor to use powerful post‑judgment tools, including bank-account garnishment and liens on non‑exempt property.

Justice courts handle smaller legal claims, usually under $20,000, while county and district courts handle higher amounts. No matter which court your case is in, you should talk with a Texas attorney promptly after receiving court papers so you do not miss your Answer deadline.

Default Judgments and Their Impact

A default judgment lets the court assume the lawsuit’s allegations are true because you did not respond. The plaintiff often receives everything requested in the petition, including the claimed balance, court costs, and sometimes attorney’s fees and interest.

This can be especially damaging in cases involving unpaid credit cards, personal loans, auto deficiencies, or medical bills—where interest and fees can grow quickly. Once the judgment is signed, reversing it is much harder and usually requires a specific legal basis and strict timelines.

If you have been properly served, it is critical to seek the advice of a Texas attorney as soon as possible. A lawyer can explain court orders, help you understand the judgment, and discuss options to attack, settle, or manage it.

Wage Garnishment and Bank Levies

When a creditor gets a default judgment against you in Texas, one of the most common ways to collect is through your bank accounts. The creditor may file a separate garnishment action asking the court to freeze and seize funds in your checking or savings accounts.

Texas law offers strong protection for most wages from garnishment on consumer debts such as credit cards, medical bills, and personal loans. However, the money you deposit into a bank account can still be at risk, and certain types of debts—like child support, spousal support, some federal student loans, and taxes—are treated differently.

What Texas Usually Protects:

- Wages for most consumer debts, including credit card debt

- Wages owed for many medical bills

- Wages from most personal loans and similar consumer accounts

What Texas Does NOT Protect:

- Your bank accounts – often the main post‑judgment target for creditors

- Wages for child support or alimony obligations

- Wages for certain federal student loans or taxes

Risks of Bank Levies in Texas:

- Bank-account garnishment is one of the most common ways creditors collect on Texas judgments.

- Creditors can freeze your checking and savings accounts, sometimes at multiple banks at once.

- Funds can be seized with little warning after the garnishment papers are served on your bank.

- Protected funds (such as certain benefits) may still be frozen until exemptions are claimed.

Other Important Texas Judgment Facts

- A Texas judgment usually lasts for 10 years and can often be renewed for additional 10‑year periods.

- Judgments can appear on your credit history and make it harder to obtain housing, loans, or favorable interest rates.

- Post‑judgment interest can cause the amount you owe to grow over time if it is not resolved.

Because most wages for consumer debts are protected in Texas, creditors often focus on bank accounts and non‑exempt property after obtaining a judgment. Ignoring the lawsuit makes it much easier for them to take these steps against you.

Property Liens

In most cases, creditors cannot force the sale of your Texas primary residence to collect on a typical consumer judgment because of strong homestead protections. However, a creditor can file an abstract of judgment in the county where you own real property. This can attach a lien to your home or other real estate, clouding the title and making it harder to sell or refinance until the judgment is resolved.

Judgments can also affect your broader financial life, including other property, vehicles, and future plans. If you are considering bankruptcy because of overwhelming debt or a judgment, be sure to consider how it may impact any cosigners.

Damage to Your Credit Report

A default judgment can severely damage your credit profile. It may show up in background or credit reports and affect your ability to get credit, rent housing, or sometimes even pass certain employment screenings. Ignoring the case does not keep it off your record—it usually makes the outcome worse.

Responding to a Debt Collection Lawsuit in Texas

Take being sued seriously, even if you think the lawsuit is wrong or you cannot afford to pay the full amount. At a minimum, you should talk with a Texas debt collection defense attorney about your options and deadlines.

Ignoring the claim is not a strategy. Even if you hope to settle or file bankruptcy later, you usually still want to file a timely Answer to avoid a default judgment and preserve your rights.

Don’t Wait—Respond Promptly

Time is critical once you are served. Use the deadlines in the Quick Answer table above to calendar your Answer due date. Missing it can lead straight to a default judgment, even if you would have had strong defenses.

Step-by-Step: How to Respond to a Texas Debt Collection Lawsuit

Here is a general, high‑level roadmap Texans can use after being served with a consumer debt lawsuit (this is not a substitute for individual legal advice):

- Read the citation and petition carefully. Confirm who is suing you, the amount they claim you owe, and which Texas court is handling the case.

- Confirm your Answer deadline. Determine whether your case is in justice court (typically 14 days from service) or county/district court (generally 10:00 a.m. on the Monday next after 20 days) and mark the date on your calendar.

- Gather your documents. Collect account statements, letters or emails from the creditor or debt buyer, any past settlement offers, and your own notes about the account.

- Talk with a Texas debt defense attorney. A lawyer can help you evaluate defenses such as mistaken identity, the wrong balance, lack of proof of ownership, arbitration clauses, or an expired statute of limitations.

- Prepare and file your Answer. File a written Answer with the correct court by the deadline, even if you cannot pay the debt. In many cases you do not have to explain everything in the Answer itself to avoid default.

- Plan your next step. Depending on your situation, that may include defending the case, negotiating a settlement, asserting arbitration, or exploring bankruptcy and other debt‑relief options.

What If You Can’t Afford to Pay the Debt?

Many Texans assume that if they cannot pay the full amount, there is no point responding. The opposite is true. Filing an Answer can keep a default judgment off your record while you explore defenses and options like settlement, payment plans, arbitration, or bankruptcy. A Texas debt collection defense attorney can help you choose the path that fits your budget and long‑term goals.

Exploring Your Options

Ignoring a debt collection lawsuit closes doors. Responding on time keeps more tools on the table to protect your income, property, and credit.

Broadly, most people facing a Texas debt collection lawsuit will consider some combination of the options below. The right solution depends on your income, assets, the type and age of the debt, and your broader financial picture.

|

Option |

Description |

|---|---|

|

Defending the lawsuit |

You file an Answer and, often with the help of an attorney, force the creditor to prove its case. Defenses can include the wrong balance, lack of documentation, ownership issues, arbitration clauses, or an expired statute of limitations. In some cases, this can lead to dismissal or a much better outcome. |

|

Negotiating a settlement |

You or your attorney work directly with the creditor to reach a settlement. This may involve a lump‑sum payment, structured payments, or a reduced balance in exchange for dismissing the lawsuit or satisfying the judgment. Settlement is often easier to negotiate before a default judgment is entered. |

|

Filing for bankruptcy |

In some situations, bankruptcy can stop debt collection lawsuits and discharge eligible debts, but it has significant long‑term effects on your credit and finances. It should be considered only after understanding all other options and how bankruptcy would affect any cosigners or non‑exempt property. |

Negotiating a Settlement

In many Texas debt cases, settlement is possible. Negotiating through an attorney can help you avoid saying or signing things that hurt your position and can improve the terms offered. In some situations, you may be able to settle for less than the full balance or spread payments out over time.

Filing for Bankruptcy

Bankruptcy is a powerful tool, but it is not right for everyone. For some people, especially those with multiple lawsuits or overwhelming debt, a Chapter 7 or Chapter 13 bankruptcy may stop collection actions and provide a fresh start. Because the consequences are serious and long‑lasting, talk with a bankruptcy attorney about how a filing would affect your assets, income, credit, and any cosigners before deciding.

Whether you defend the lawsuit, negotiate a settlement, or consider bankruptcy, the key is to act before a default judgment is entered—or as soon as you learn a judgment already exists.

Frequently Asked Questions

What happens when you ignore being sued for debt in Texas?

If you ignore a Texas debt collection lawsuit, the court can enter a default judgment after your Answer deadline passes. The judge may assume the allegations in the petition are true and award the creditor what it requested, including the claimed balance, court costs, and sometimes attorney’s fees and interest. That judgment can last for years, damage your credit, and allow the creditor to pursue post‑judgment remedies like bank-account garnishment and property liens.

What happens if you don’t show up to a lawsuit hearing in Texas?

If you do not appear when your Texas case is set for a hearing, and you have not filed a proper Answer, the court may enter a default judgment against you. Even if you filed an Answer, missing a trial or key hearing can result in important rulings being made without your input and can seriously weaken your position. Always talk with the court or a lawyer before missing a scheduled appearance.

What happens if a company you sue in Texas doesn’t respond?

If you sue a company in Texas and it is properly served but does not respond by the deadline, you may be able to seek a default judgment against the company. The court will require proof that the company was served correctly and that your petition supports the relief you are requesting before signing a default judgment.

What happens if you don’t pay a judgment from a lawsuit?

If you do not pay a judgment from a Texas lawsuit, the creditor can take additional steps to collect. These may include bank-account garnishment, abstracts of judgment that create liens on non‑exempt real property, post‑judgment discovery about your assets, and continued accrual of post‑judgment interest. While most wages for consumer debts are protected, your bank accounts and non‑exempt property can still be at risk.

What if I already have a default judgment against me in Texas?

If you already have a default judgment in Texas, you may still have options, but they are time‑sensitive. In some cases, you may be able to file a motion to set aside or attack the judgment based on service problems or other legal issues, or you may be able to negotiate a settlement or consider bankruptcy. Because the rules and deadlines are strict, it is important to speak with a Texas attorney quickly if you discover a judgment against you.

Conclusion: Don’t Ignore a Texas Lawsuit

Understanding the consequences of ignoring a lawsuit—especially a debt collection lawsuit in Texas—is vital. Ignoring the case does not make it go away; it usually leads to a default judgment, long‑term financial fallout, and a harder path to fixing the problem.

By responding on time, you preserve the ability to dispute the debt, negotiate a settlement, assert defenses like arbitration or limitations, or explore bankruptcy and other relief. Consulting a Texas attorney early gives you the chance to review your options, understand the procedures in justice, county, or district court, and make informed decisions.

In many Texas debt collection cases, that means filing an Answer within 14 days in justice court or by 10:00 a.m. on the Monday next after 20 days in county or district court, depending on where the lawsuit was filed. Missing those deadlines could result in a default judgment that affects your bank accounts, property, and credit for years.

Important disclaimer: This article is for informational purposes only, is based on Texas law, and does not constitute legal advice for your specific situation. Reading this page does not create an attorney–client relationship, and results cannot be guaranteed. Always consult directly with a licensed Texas attorney about your own case and deadlines.

If you have been sued for a debt in Texas—or learned that a default judgment already exists—our team is here to help you understand your options. During a free consultation, we can review your situation, discuss possible defenses and strategies, and help you choose the next step.

Call us at (888) 584-9614 or contact us online to start planning your response today.