Quick Answer: Your Chances of Winning a Credit Card Lawsuit in Texas

Reviewed by: Christopher Migliaccio, Managing Partner • Updated: Nov. 6, 2025

We help Texans beat credit card lawsuits by filing timely Answers and raising proven defenses. Call (888) 584-9614 for your free consultation.

- JP Court: File Answer within 14 days (TRCP 502.5)

- County/District: File by Monday after 20 days at 10 a.m. (TRCP 99(b))

- Key Defense: 4-year statute of limitations (Tex. Civ. Prac. & Rem. Code § 16.004)

- Outcomes: Defendants who respond and assert defenses often secure dismissals or more favorable settlements; defaults are common when no Answer is filed.

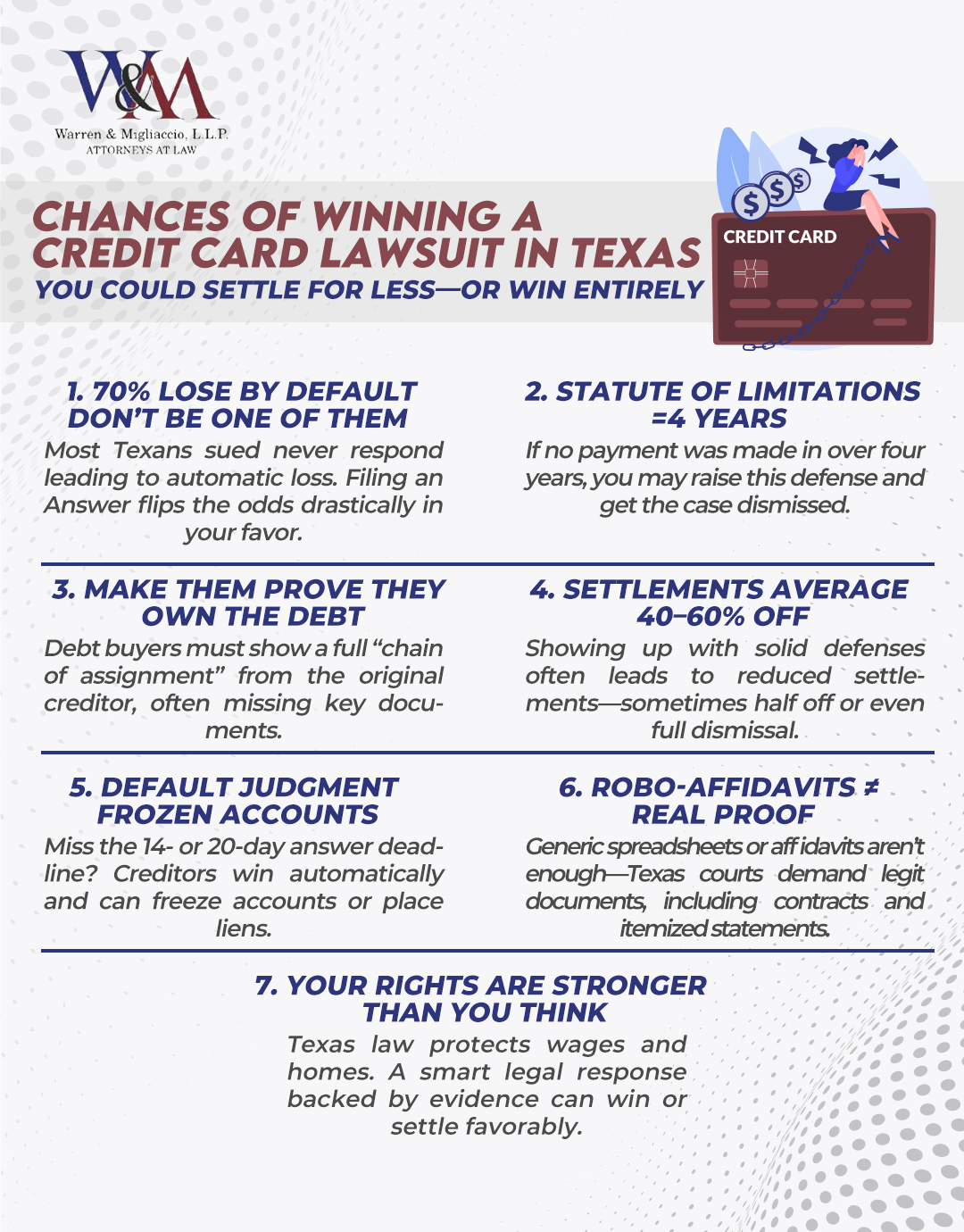

Texas consumers who file a timely Answer, which is your written response to a lawsuit, and raise defenses like the four-year statute of limitations often put themselves in a stronger position to seek dismissal or negotiate a better settlement. If you miss the Answer deadline—14 days in justice court or by 10:00 a.m. on the Monday after 20 days in county or district court—the plaintiff may request a default judgment, which is a judgment entered because no Answer was filed. Defaults are common when defendants never respond. Tex. R. Civ. P. 99(b); Tex. R. Civ. P. 502.5.

Being served with a credit card lawsuit feels overwhelming, especially for those unfamiliar with Texas court procedures. After several months of non-payment, creditors or debt buyers may sue to recover the debt. Yet across Texas, we see consumers who show up and assert proper defenses often walk away paying far less—or nothing at all. Understanding what happens when a credit card company sues you in Texas helps you prepare an effective defense.

Warren & Migliaccio helps families statewide fight credit card lawsuits. Since 2006, we’ve protected what matters most for Texas families facing debt collection. Call (888) 584-9614 for your free consultation.

Why Credit Card Companies Sue—and What Affects Outcomes

📊 Debt Lawsuit Dynamics in Texas

| Plaintiff Type | Typical Documentation Posture | When You Respond & Challenge |

|---|---|---|

| Original Creditors (Chase, Capital One, etc.) |

Often have more complete records | Proof still must be authenticated; outcomes improve when documentation is scrutinized |

| Debt Buyers (Midland, Portfolio Recovery, etc.) |

Documentation can be incomplete or inconsistent | Challenging the chain of assignment and accuracy often leads to dismissals or better settlements |

Key Insight: Filing an Answer forces the plaintiff to prove every element with admissible evidence.

The plaintiff has the burden to prove it owns the account and the amount it claims you owe. Filing an Answer keeps the case contested, which means a debt buyer may have to prove the chain of assignments from the original creditor to the current plaintiff. When the plaintiff can’t prove ownership or the balance with admissible evidence, dismissal or a settlement on better terms is more likely. Absolute Resolutions Invs., LLC v. Cureton, 497 S.W.3d 332 (Tex. App.—Dallas 2016).

Common Lawsuit Triggers in Texas

- Account charged-off and sold to a debt buyer

- No payments for several months

- Approaching the 4-year statute of limitations deadline

- Higher balances (varies by plaintiff policy)

⚠️ Christopher Migliaccio’s Insight

I’ve seen hundreds of Texas families face credit card lawsuits since 2006. The biggest mistake? Ignoring the citation. In my experience, debt buyers often can’t produce the original contract or complete chain of ownership. One client faced a $12,000 Midland Funding suit. We demanded proof of assignment—they had none. Case dismissed. The lesson: force them to prove every element. Many can’t.

—Christopher Migliaccio, Managing Partner, Warren & Migliaccio, L.L.P.

Four Proven Texas Defenses That Win Credit Card Cases

Texas law provides powerful defenses against credit card lawsuits. The four-year statute of limitations under Tex. Civ. Prac. & Rem. Code § 16.004 often defeats old claims. Debt buyers frequently lack proper documentation to establish standing. We use these defenses to negotiate dismissals or substantial reductions for our clients statewide.

Defense Checklist—Check All That Apply:

- ☐ Last payment more than 4 years ago

- ☐ No complete chain of assignment shown

- ☐ Fees not matching original agreement

- ☐ Prior settlement or bankruptcy discharge

- ☐ Wrong person sued (identity theft/error)

Checking even one box may provide a winning defense. We analyze every angle to maximize your leverage.

Critical Texas Deadlines That Determine Your Case

🚨 Texas Answer Deadlines—Don’t Miss These!

| Court Level | Deadline | Rule |

|---|---|---|

| Justice of the Peace (JP) | 14 calendar days from service date | TRCP 502.5 |

| County/District Court | Monday after 20 days by 10:00 a.m. | TRCP 99(b) |

Miss the deadline = Automatic loss by default judgment

How to File Your Answer in Texas Courts

- Draft your Answer: Deny allegations and list all defenses

- File with court clerk: In person or e-file before the deadline

- Serve plaintiff’s attorney: Send copy by certified mail or e-service

- Request discovery: Demand proof of debt ownership and amount

Pro Tip: In county and district court, Texas Rule of Civil Procedure 194 requires each side to exchange initial required disclosures early in the case, including the legal theories and the basic information and documents they may use. Tex. R. Civ. P. 194.2.

Settlement vs. Trial—What Texas Families Actually See

✓ Lump Sum Settlement

Pros: Often a larger discount; case ends immediately

Cons: Requires funds up front

Best for: Those with available savings or approved financing

✓ Payment Plan

Pros: Manageable monthly payments

Cons: Longer commitment; higher total paid in many cases

Best for: Steady income, limited savings

We negotiate both options for clients. Your leverage depends on the plaintiff’s documentation and your defenses.

FDCPA & Texas Debt Collection Act Violations That Flip Cases

We regularly uncover violations that transform defendants into plaintiffs:

- Robo-signed affidavits: Invalid testimony with wrong amounts

- Illegal contact: Calls after 9 p.m. or to your workplace after notice

- False threats: Claiming wage garnishment for credit card debt (Texas generally bars wage garnishment for consumer debts, with limited exceptions like court-ordered child support). Tex. Const. art. XVI, § 28.

- Wrong defendant: Suing victims of identity theft

- Time-barred suits: Filing after the 4-year limitations period expires

Under the FDCPA, a consumer can recover actual damages and may recover up to $1,000 in statutory damages per lawsuit, plus reasonable attorney’s fees and costs. Texas law can allow additional damages depending on the facts and the remedy being pursued. 15 U.S.C. § 1692k(a).

Texas Case Law: Why Debt Buyers Often Lose

Texas courts require a debt buyer to prove it owns the account with competent evidence tracing the assignments from the original creditor to the current plaintiff. Absolute Resolutions Invs., LLC v. Cureton, 497 S.W.3d 332 (Tex. App.—Dallas 2016).

—Absolute Resolutions Invs., LLC v. Cureton, 497 S.W.3d 332 (Tex. App.—Dallas 2016)

In Cureton, the Dallas Court of Appeals affirmed dismissal when a debt buyer presented only generic billing records without proving the complete chain of ownership. We cite this case regularly when challenging debt buyer lawsuits. Courts require authenticated purchase agreements, not just spreadsheets.

Recent example: Discover Bank v. Marcus Miller, No. 01-23-00513-CV, 2025 WL 2109891 (Tex. App.—Houston [1st Dist.] July 29, 2025) was an arbitration decision in a consumer loan dispute, not a ruling about proving debt ownership in a credit card case. Discover Bank v. Marcus Miller, No. 01-23-00513-CV, 2025 WL 2109891 (Tex. App.—Houston [1st Dist.] July 29, 2025).

When Chapter 7 Bankruptcy Provides a Fresh Start

For North Texas families facing multiple lawsuits, Chapter 7 bankruptcy may offer the cleanest solution. The automatic stay under 11 U.S.C. § 362 immediately stops all collection lawsuits, garnishment attempts, and creditor calls the moment we file.

- Automatic stay: Halts all collection actions instantly

- Texas exemptions: Protect your homestead, vehicles, retirement accounts

- Quick discharge: Typically complete in about 120 days

- No wage garnishment: Texas generally bars wage garnishment for consumer debts like credit card judgments. Tex. Const. art. XVI, § 28.

We handle Chapter 7 cases in Dallas, Collin, Denton, Rockwall, and Tarrant Counties. Free bankruptcy consultation: (888) 584-9614.

Common Mistakes Texas Consumers Make

- Ignoring the lawsuit: Guarantees default judgment

- Admitting the debt: If a debt buyer’s lawsuit is time-barred, Texas law says the claim is not revived by an oral or written reaffirmation of the debt. Tex. Fin. Code § 392.307(d).

- Making small “good-faith” payments: If a debt buyer’s lawsuit is time-barred, Texas law says the claim is not revived by a payment on the consumer debt. Tex. Fin. Code § 392.307(d).

- Skipping mediation or court dates: Same risk as missing trial

- Going alone: Missing critical defenses or deadlines

Don’t make these mistakes. Call Warren & Migliaccio at (888) 584-9614 before these traps cost you thousands.

Frequently Asked Questions About Credit Card Lawsuits in Texas

Chances & Winning Strategies

What are the chances of winning a credit card lawsuit in Texas?

Defendants who file timely Answers and raise defenses often secure dismissals or better settlements. Many cases end in default only because no Answer is filed. Your chances improve by:

- Filing an Answer within 14 days (JP) or by the Monday after 20 days (County/District)

- Raising the 4-year statute of limitations defense when it applies

- Challenging the chain of assignment and the amount claimed

How do you win a credit card lawsuit in Texas?

File an Answer denying claims and assert defenses like limitations, lack of standing, incorrect amount, and identity issues. This shifts the burden to the creditor to prove every element with admissible records.

- Gather statements showing your last payment date

- Request the complete chain-of-assignment documents

- Negotiate settlement if defenses are weak

Consequences & Evidence

What happens if you ignore a credit card lawsuit in Texas?

Ignoring a lawsuit typically results in a default judgment for the full amount plus court costs. A judgment creditor can freeze bank accounts and place liens on non-exempt real property. Texas generally prohibits wage garnishment for consumer credit-card debt.

What evidence does a debt collector need to win in Texas?

They must prove ownership via a complete chain of assignment from the original creditor, a valid agreement, account statements, and a correct balance with interest/fee calculations. Missing elements often force dismissal or settlement.

Settlement, Time Limits & Garnishment

Can you settle a credit card lawsuit after being served in Texas?

Yes. You can negotiate at any point before judgment—file your Answer first to keep leverage. Strong defenses often yield better terms. Get all terms in writing with dismissal “with prejudice.”

How long do creditors have to sue for credit card debt in Texas?

Most claims must be filed within four years of default or last payment (Tex. Civ. Prac. & Rem. Code § 16.004). If limitations expired before filing, raise it in your Answer for dismissal.

Can wages be garnished for credit card debt in Texas?

No. Texas Constitution Article XVI, Section 28 generally prohibits wage garnishment for consumer debts. After judgment, creditors may seek bank-account garnishment and liens on non-exempt property; certain funds are exempt by law.

Defenses, Deadlines & Bankruptcy

What defenses help win a credit card debt lawsuit in Texas?

Strong Texas defenses include the four-year statute of limitations, lack of standing without ownership proof, incorrect amount owed, and prior settlement or bankruptcy discharge. Any viable defense forces real proof.

What happens if you miss the answer deadline in Texas?

Missing the 14-day JP or Monday-after-20-days County/District deadline can lead to a default judgment. File your Answer as soon as possible after you are served to preserve defenses. Tex. R. Civ. P. 99(b); Tex. R. Civ. P. 502.5.

Does bankruptcy stop a credit card lawsuit immediately?

Yes. Filing Chapter 7 triggers the automatic stay under 11 U.S.C. § 362, which immediately halts lawsuits, bank levies, and collection calls nationwide.

Take Action Now—Protect Your Rights

Texas consumers who respond to credit card lawsuits and assert proper defenses dramatically improve their chances of winning or settling favorably. Since 2006, Warren & Migliaccio has helped families statewide beat debt collection lawsuits and protect what matters most.

Don’t become another default judgment statistic. We provide free consultations to review your case and explain your options. Our Lead Counsel Verified attorneys know how to challenge creditors and debt buyers who can’t prove their claims.

Call (888) 584-9614 today or contact us online for your free consultation. Our experienced Texas debt lawsuit defense lawyers serve clients statewide with proven strategies that work.

Free Consultation—No Obligation

Facing a credit card lawsuit? We can help you fight back.

Serving all of Texas • Offices in Dallas-Fort Worth

Information only; not legal advice. Past results do not guarantee outcomes.