If you’ve ever wondered whether you could keep a credit card out of a chapter 7 bankruptcy to preserve your credit line, you’re not alone. Many people facing overwhelming debt hope to keep at least one credit card as a backup. However, can I exclude a credit card from Chapter 7 bankruptcy? The short answer is no. Bankruptcy law requires you to disclose all credit card accounts and debts. Public records of bankruptcy are compiled by national credit bureaus, which can impact a debtor’s credit report and overall credit recovery process after bankruptcy. This article explains why excluding a credit card isn’t possible, the consequences of trying to do so, and the options you have moving forward.

The Data Behind “Can I Exclude a Credit Card from Chapter 7 Bankruptcy?”

According to the United States Courts, more than 360,000 chapter 7 bankruptcies were filed in the U.S. in a recent year, and credit card balances were among the most common types of debts. This shows how regularly unsecured creditors, such as credit card companies, show up in these cases.

Why does this matter? It reveals that nearly everyone who decides to file chapter 7 must list every card in their bankruptcy forms. If you try to exclude one for convenience or future use, it can threaten the fairness of the case. By looking at the numbers, you see how critical it is to disclose every single credit card account.

360,000

Total Filings

65%

CC Debt Cases

30%

Medical Bills

Understanding Chapter 7 Bankruptcy and Credit Card Debt

Chapter 7 bankruptcy offers a fresh start by wiping out most unsecured debts, including credit card debt. When you file, an automatic stay stops most creditor collection efforts, giving you time to catch your breath. It’s a chance to reset your finances and begin again without the weight of old debts. For more details on how this process works, see https://www.consumerfinance.gov/ask-cfpb/can-a-debt-collector-increase-the-interest-rate-on-a-debt-i-owe-en-1417.

However, your credit account will likely be closed once you file. Credit card issuers usually shut down any open cards, even those with zero balance. Since credit card debt is dischargeable—unless there is fraud or misrepresentation—the goal is to let you rebuild your finances free from past burdens.

So, what happens next? Any credit card debts you have will be cleared, and you can start rebuilding credit. But it’s important to understand why you must disclose all cards and how the bankruptcy trustee fits into the picture.

Related Guide: Filing Chapter 7: What Happens to My Cosigner?

Anecdote: A Hypothetical “Car Loan” Twist

Imagine Alicia, a Texas resident with multiple credit cards and a car loan. Worried about foreclosure on her home, she sought help from a bankruptcy lawyer at a law firm. Alicia wanted to keep one credit card account for emergencies. Yet her attorney explained that under 11 U.S.C. § 521, she had to list every debt, including the card with a zero balance. Hiding even one could lead to fraud claims. She realized that total honesty was best, so she filed all her accounts in the bankruptcy petition. Though she lost her old cards, she felt relief once her large debts—including a leftover car loan deficiency—were discharged.

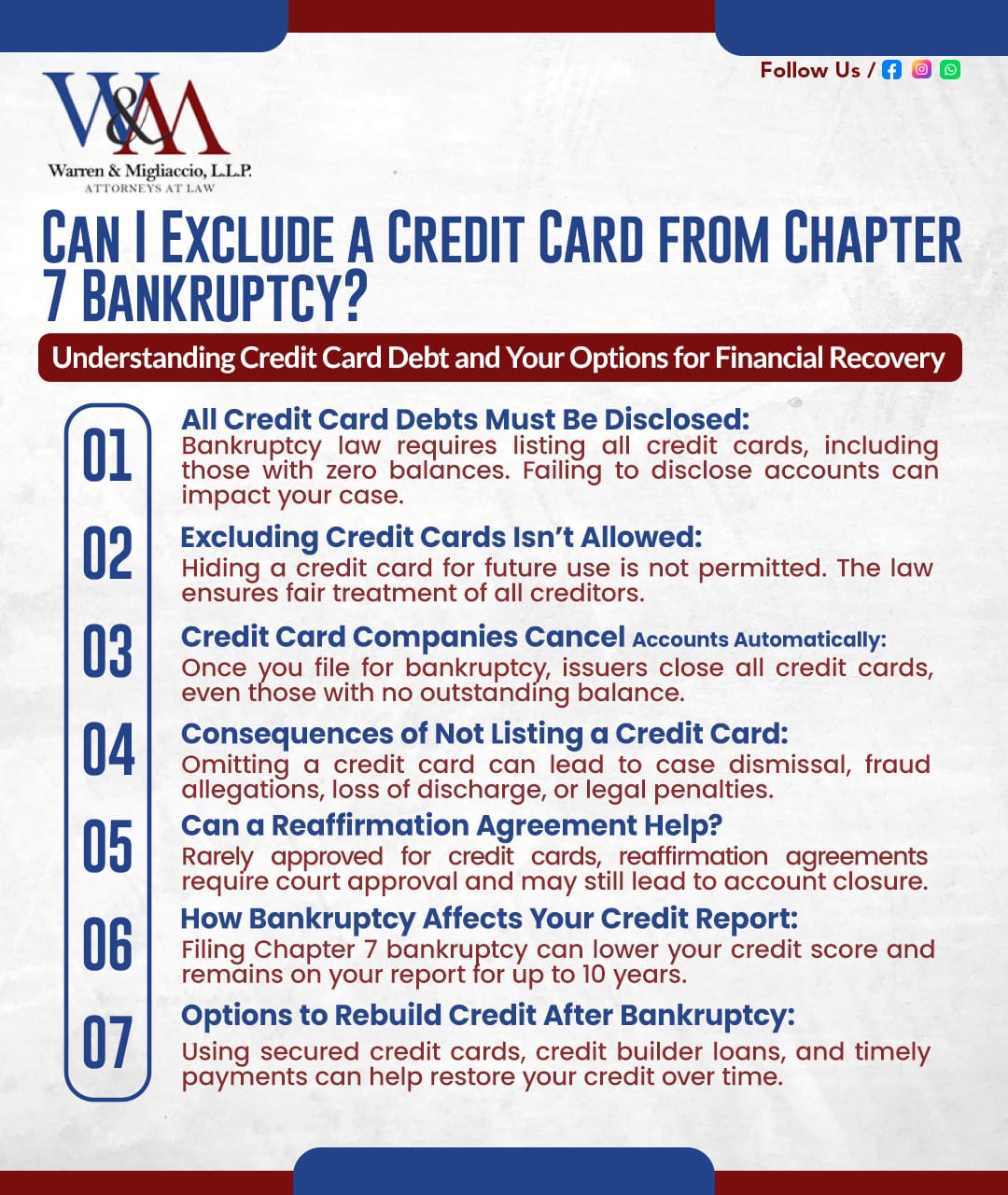

Mandatory Disclosure of All Credit Card Debts

When filing chapter 7 bankruptcy, you must list all credit card accounts. This rule applies even if your balance is zero. You should disclose:

Every credit card with an existing balance.

Every credit card with a zero balance.

Any closed card that still shows on your credit report.

Being open is crucial. If you leave something out, you can make your bankruptcy case harder for the bankruptcy trustee to handle. You could also face legal trouble for incomplete disclosure.

Why Excluding Credit Cards Isn’t Feasible

Under bankruptcy law, you cannot exclude any debts, including credit cards. The bankruptcy code requires total disclosure. Many people think they can hide a card to keep using it after bankruptcy filing, but that idea is incorrect.

Once you file chapter 7 bankruptcy, any credit card you have is likely canceled. Judges rarely approve a reaffirmation agreement for credit cards because they aren’t essential. The law wants every creditor treated equally, so excluding a card would be unfair.

Credit Card Company Actions After Bankruptcy Filing

When you file for Chapter 7 bankruptcy, credit card companies act swiftly to protect their interests. As soon as they receive notice of your bankruptcy filing, they will typically cancel all your credit card accounts, regardless of whether you have an outstanding balance or not. This immediate action is rooted in bankruptcy law, which mandates the automatic cancellation of contracts, including credit card agreements.

Credit card companies take this step to mitigate any potential risks associated with your financial situation. By canceling your credit cards, they prevent further accumulation of debt that you might not be able to repay. This also aligns with the overarching goal of bankruptcy proceedings, which is to provide a fair and equitable treatment of all creditors.

While losing access to your credit cards can be inconvenient, it’s a necessary part of the bankruptcy process. It ensures that all your debts are accounted for and that you can start fresh without the burden of old financial obligations. Understanding this can help you better navigate the challenges of bankruptcy and focus on rebuilding your credit responsibly.

The Role of the Bankruptcy Trustee

A bankruptcy trustee oversees chapter 7 bankruptcy cases to ensure compliance with bankruptcy law. This person:

Reviews your assets and liabilities, including credit card debts.

Makes sure all unsecured creditors are treated fairly.

Investigates signs of fraud or improper acts.

If you don’t disclose some of your credit card information, the trustee may not be able to notify every credit card company or handle the case properly. This can lead to serious consequences and disrupt the entire bankruptcy process.

Potential Consequences of Not Disclosing Credit Cards

Not listing all credit cards in your bankruptcy petition is just one of many mistakes to avoid before filing for bankruptcy. It can lead to:

Case dismissal: You remain on the hook for all your debts.

Fraud allegations: Intentional secrecy can bring legal penalties.

Loss of discharge: You may lose the chance to eliminate those debts.

Fines or more legal issues: Inaccurate filings can trigger extra problems.

Your best move is complete honesty. Any attempt to hide details threatens your new start and can cause you more stress later.

Reaffirmation Agreements: A Possible Exception?

A reaffirmation agreement lets you keep certain debts you would normally lose in chapter 7 bankruptcy. With credit cards, reaffirmation is rare, especially if there’s no outstanding balance. Even if it’s allowed, the card issuer might still close the account.

Reaffirming credit card debt is a legal option to exempt certain debts from discharge, but it poses significant risks. It requires court approval and may allow you to retain credit cards. However, be cautious of the burdens of high interest rates and the necessity of full disclosure of debts during bankruptcy filings.

A bankruptcy attorney can help with reaffirmation, which needs court approval. But be aware:

High interest rates often remain.

Missing payments can lead to repossession or other collection actions.

Court officials want to see that keeping this debt is in your best interest.

If you sign a reaffirmation, keep making payments on time. This can help your credit score and your payment history, but only if you’re able to handle the financial load.

Bankruptcy Truth

Hiding a credit card isn’t an option—transparency in your filing ensures fairness and legal protection.

Impact on Your Credit Report and Scores

As soon as a credit card company learns of your bankruptcy filing, it will likely close your card. This closure can lower your credit score by 100 to 240 points, depending on your past credit history.

A chapter 7 bankruptcy note stays on your credit report for up to 10 years. It’s wise to check your reports after you receive your bankruptcy discharge to ensure everything is correct. On the bright side, many people start receiving new credit card offers a few months after the bankruptcy case closes. Responsible use of these new cards can help improve your score in about two years.

Authorized User Accounts and Chapter 7 Bankruptcy

If you’re just an authorized user on someone else’s credit card account, your bankruptcy filing won’t hurt the main cardholder’s score. Authorized users aren’t liable for the debt. Still, it’s usually best to remove authorized users before filing to avoid reporting mix-ups.

Becoming an authorized user again after bankruptcy can help rebuild your credit history. You won’t need a credit check, which makes it a useful strategy if you need to increase your credit score.

Options for Rebuilding Credit After Chapter 7 Bankruptcy

You can rebuild credit more easily than you might think. Soon after your bankruptcy discharge, you may see new credit card offers. Some people start with a secured credit card, which requires a deposit:

Keeping a strict budget and paying bills on time are key steps in strengthening your credit. Using secured credit cards responsibly to establish a positive payment history can improve credit scores and facilitate access to better credit offers in the future. Within about two years of consistent, responsible behavior, many people see meaningful score improvements.

Interesting Credit Card Debt stats related to bankruptcy filings

In 2021, consumer bankruptcy filings in the U.S. included a large portion tied to credit card debt.

Around 65% of chapter 7 bankruptcy cases in 2020 listed credit card debt as the main financial problem.

Over 30% of filers said unexpected medical bills played a part in their credit card debt.

People between 25 and 34 years old are among the most likely to file due to heavy credit card burdens.

These stats show how serious credit card debt can be and why so many turn to debt relief through bankruptcy.

Mandatory Disclosure

Leaving out even a zero‑balance card can trigger fraud allegations and risk your entire filing.

Consulting with a Texas Bankruptcy Attorney

Talking to a Texas bankruptcy attorney is an important step. Many offer a free consultation or apply the fee toward future legal advice. Prepare by collecting:

A list of all your debts.

Recent statements for all credit cards and other loans.

Any credit report you’ve obtained.

An experienced attorney from a well-regarded law firm can explain the bankruptcy code and bankruptcy court process. They can also advise on chapter 13 bankruptcy if a repayment plan is better for your financial situation. They’ll look at different types of bankruptcy and guide you through handling secured debts like a car loan versus unsecured debts like credit cards.

You don’t have to hire the first attorney you speak with—ask questions, take their phone number, and check references. Having professional help can ease a stressful time.

Full Disclosure is Crucial

Every credit card—even those with zero balances—must be listed to protect your case from severe legal repercussions.

FAQs Regarding: Excluding or Not Disclosing Credit Cards

Frequently Asked Questions

Excluding or Not Disclosing Credit Cards

Can I Legally Keep a Credit Card Out of My Chapter 7 Bankruptcy Filing?

It is not legally possible to exclude any credit card when filing for chapter 7 bankruptcy. All debts must be listed to ensure complete transparency.In most cases, any attempt to omit a credit card can result in case dismissal or allegations of fraud. The bankruptcy process is designed for equitable treatment of creditors, so leaving out specific cards goes against that goal. Always include every credit card account, even if its balance is zero.

What Happens If I Don’t Disclose All My Credit Cards in a Chapter 7 Filing?

Failing to disclose all credit cards can lead to severe legal repercussions, including dismissal of your case and potential fraud allegations.Complete transparency is crucial for accurate debt evaluation. Hiding accounts can undermine the fairness of the proceedings and may result in your debts staying enforceable after the case ends.

Is It Fraud to Hide a Credit Card in Bankruptcy?

Yes, intentionally failing to report or hiding a credit card is considered bankruptcy fraud. Fraud can lead to having your case dismissed and possibly facing criminal consequences.Courts require total honesty to ensure fair treatment for all unsecured creditors. Trying to hide a card breaks that rule and endangers your fresh start.

Can Authorized User Accounts Be Excluded from Chapter 7?

Authorized user accounts usually don’t have to be listed as debts because you’re not the primary cardholder. However, it’s smart to list them anyway for correct reporting.Removing your name as an authorized user before filing can prevent confusion on credit reports. Because you’re not legally responsible for the debt, it helps clarify liability during and after the bankruptcy case.

Credit Cards After Filing Chapter 7

What Happens to My Credit Cards Once I File for Chapter 7 Bankruptcy?

Once you file for chapter 7 bankruptcy, your credit card issuers will likely close your cards, even if you have no outstanding balance. This is because your credit relationship typically ends once bankruptcy proceedings begin.

Can I Keep Any Credit Cards After Filing for Chapter 7 Bankruptcy?

Most credit cards are closed once you file. You might be able to keep one if a reaffirmation agreement is approved, but this is rare.Courts often consider credit cards unnecessary, making them unlikely to support a reaffirmation. In most cases, you’ll need to find new credit options after discharge.

How Does Reaffirmation Work for Credit Card Debt in Chapter 7 Bankruptcy?

Reaffirmation allows you to keep certain debts by agreeing to pay them even after discharge. This is uncommon with credit cards since they’re unsecured debts.If a reaffirmation is approved, you continue making payments on that card. The court must confirm it serves your best interest, given the high interest rates credit cards often have.

Will My Credit Card Issuer Cancel My Account Even If I Have a Zero Balance?

Yes. Most card issuers will cancel your account once they learn you’re filing for chapter 7 bankruptcy, regardless of the balance.They prefer avoiding any future risk. Though losing your accounts can feel discouraging, many people rebuild credit soon after with new cards or secured credit cards.

Filing & Trustee

What Is the Role of the Bankruptcy Trustee Regarding Credit Card Debts?

A bankruptcy trustee makes sure all debts, including credit card debts, are fully disclosed and handled correctly. They gather and distribute any nonexempt assets to creditors.The trustee also checks for fraud or missing information. Their main task is to ensure every creditor is treated fairly and the bankruptcy code is followed.

Do They Freeze Your Bank Account When You File Chapter 7?

Usually, your bank account is not automatically frozen. However, if you owe that same bank money or there’s possible fraud, it might place a temporary hold.To avoid issues, tell your bank about your bankruptcy filing and keep track of your account activity.

What Happens If You Forgot to List a Creditor in Chapter 7?

You can often amend your bankruptcy petition to add a missing creditor. Not doing so can leave you liable for that debt and potentially lead to legal trouble.Always check your credit report and financial records to ensure you list everyone you owe.

What Not to Do When Filing Chapter 7?

Avoid new debt, asset transfers, or hiding financial details after deciding to file. Such actions can lead to fraud claims or having your bankruptcy case thrown out.Keep clear, honest records and always seek legal advice before big financial moves.

Should I File Chapter 7 Bankruptcy?

Chapter 7 bankruptcy can help if you meet the means test and have difficulty paying debts like credit card debt. It’s best for those with little disposable income who need an immediate break from unmanageable bills.Consult a bankruptcy attorney to check if this is right for your situation. They’ll see if you qualify and help you weigh alternatives like chapter 13 bankruptcy.

Credit Score & Rebuilding

How Can I Rebuild My Credit After Chapter 7 Bankruptcy?

Apply for secured credit cards, consider credit builder loans, and pay any new credit on time. This approach helps restore trust with lenders.Sticking to a budget, paying bills punctually, and monitoring your credit report are essential parts of the rebuilding process.

How Long Does a Chapter 7 Bankruptcy Affect My Credit Score?

A chapter 7 bankruptcy can stay on your credit report for up to 10 years. It may lower your score right away.The actual drop depends on your credit history and how much debt gets discharged. Many people see their score improve in about two years through careful financial management.

How Soon Can I Get a New Credit Card After Chapter 7 Discharge?

Some people get new credit card offers within months of chapter 7 bankruptcy discharge.Secured credit cards are usually the first option. By paying on time and keeping balances low, you can strengthen your score more quickly.

Are There Ways to Protect My Credit Score While Filing for Chapter 7?

You can reduce the hit by avoiding late payments before filing and checking your credit reports for mistakes. Although your score will go down, good habits can lessen the blow.Focus on steady income, limit new debt, and explore credit counseling. Over time, consistent efforts can speed up recovery.

Bankruptcy Qualifications & Legal Assistance

How Do I Qualify to Discharge Credit Card Debt in Chapter 7 Bankruptcy?

You generally need to pass the means test, which compares your income to your state’s median. If you fall below the limit, you’re more likely to qualify.A bankruptcy attorney can help verify the details of your household income, deductions, and allowable expenses.

Will My Credit Card Balances Get Paid in Chapter 7 Bankruptcy?

In chapter 7, credit card balances are mostly discharged, not “paid.” That means you don’t owe them anymore.Fraud or major luxury purchases can affect discharge, so consult an attorney for specifics.

How Can a Bankruptcy Attorney Help?

A bankruptcy attorney assists with paperwork, deadlines, and important decisions like reaffirmation agreements or when to file.Their guidance lowers the chance of mistakes that might delay or jeopardize your discharge.

Real-World Case Study: “How Was a Car Loan Reaffirmation Handled in a Hypothetical Chapter 7 Case?”

Picture Jonah, who owed $10,000 on a car loan at 12% interest and also had large credit card balances. Filing for chapter 7, he worried about losing his car. A bankruptcy lawyer advised reaffirming the car debt so he could keep it for work.

The bankruptcy court checked if it was wise for Jonah to keep paying a high interest rate. After discussions, the lender lowered the rate to 9%, which made the monthly payments more manageable. The reaffirmation was approved because Jonah needed the car for his job. By making on-time monthly payments, he improved his credit score and kept the vehicle. For more on reaffirmation agreements, see United States Courts Reaffirmation FAQ. Jonah’s type of bankruptcy—chapter 7—still wiped out his credit card debt without costing him his transportation.

Summary

Chapter 7 bankruptcy in Texas makes it clear that you can’t exclude any credit card debt. Bankruptcy trustee oversight, potential penalties, and rare reaffirmation agreement possibilities all play a role. You also need to think about the effects on your credit report and how to rebuild after bankruptcy.

While navigating Chapter 7 bankruptcy can feel complicated, the right preparation and a skilled bankruptcy attorney can make a big difference. A well-planned legal strategy ensures you fully disclose your debts, keep the process fair, and move toward a more stable financial future.

If you’re looking for guidance, our experienced estate planning attorneys in Texas can help you create a plan that protects your assets and secures your future. Call us at (888) 584-9614 or contact us online to discuss your situation and take the next step toward financial stability.

Disclaimer: This article is for informational purposes only and does not constitute legal advice.