In Texas, filing bankruptcy can wipe out many unsecured debts, stop most collection actions, and give you a structured path to rebuild. However, it can harm your credit, risk some non-exempt assets, and will not erase every type of debt. That’s why it’s important to evaluate all the factors carefully.

Deciding whether to file for bankruptcy is challenging. If you’re struggling with overwhelming debt, it’s important to weigh the pros and cons before you file. Texas laws regarding bankruptcy are complex and can have long-term financial and personal consequences, so it’s important to understand your options before taking the next step.

Quick Answer: What are the main pros and cons of filing bankruptcy in Texas?

In Texas, bankruptcy may help you eliminate overwhelming debt and stop collections, but you should review exemptions, deadlines, and alternatives with a local attorney before deciding if filing makes sense.

- List your debts, income, and essential assets.

- Compare Chapter 7 and Chapter 13 pros and cons.

- Schedule a free consultation with a Texas bankruptcy lawyer.

As a bankruptcy lawyer and co-founder of Warren & Migliaccio, L.L.P., I have helped countless clients navigate bankruptcy proceedings. Our firm specializes in Chapter 7 filings, and our team has years of experience helping individuals and families in Texas get back on their feet.

Need-to-Know Highlights

- Bankruptcy can erase many unsecured debts but cannot eliminate all obligations.

- Texas exemptions strongly protect homesteads, basic personal property, and retirement accounts.

- Bankruptcy damages credit but often creates a workable path to rebuild over time.

- Chapter 7 and Chapter 13 serve different goals and financial situations.

- A Texas bankruptcy lawyer can explain options and help avoid costly mistakes.

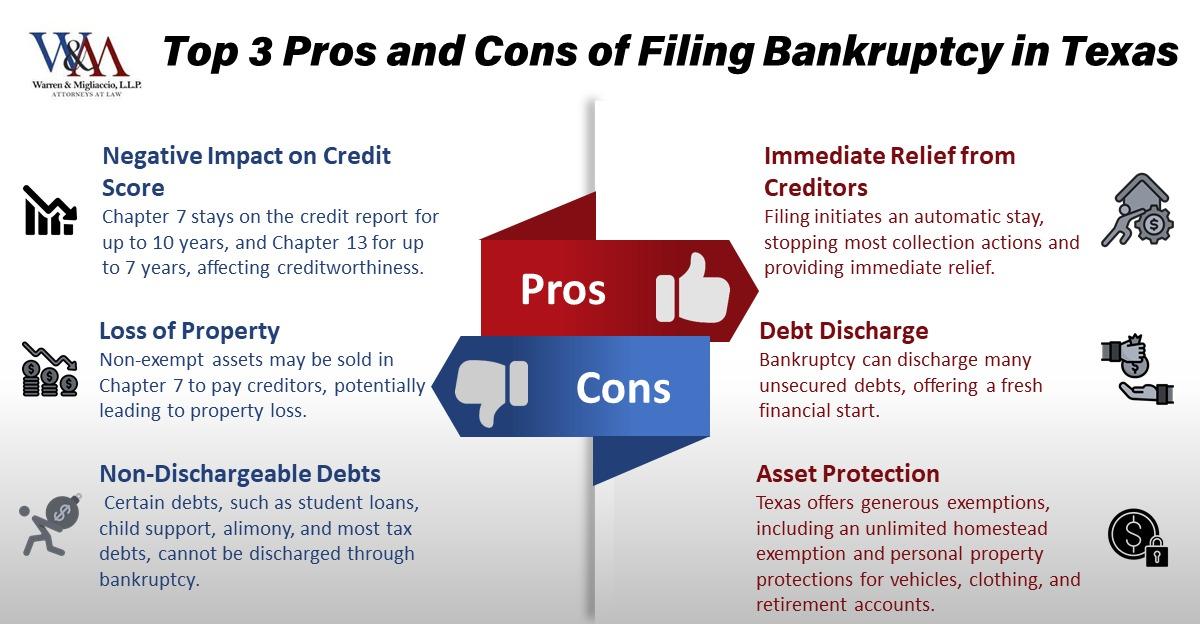

Pros of Filing for Bankruptcy

When considering bankruptcy, the potential benefits can often outweigh the drawbacks. Here are three significant advantages to filing for bankruptcy in Texas.

1. Debt Discharge or Reduction

The most obvious benefit of filing for bankruptcy is the ability to discharge or reduce your debts. In Chapter 7 bankruptcy, many unsecured debts, such as credit card debt, medical bills, and personal loans, can be wiped out in a discharge order under 11 U.S.C. § 727, but categories listed in 11 U.S.C. § 523(a)—including most student loans, certain recent taxes, and support obligations—generally remain non dischargeable debts.

In Chapter 13 bankruptcy, you enter a repayment plan but still benefit from the possibility of reducing unsecured debts. This type of bankruptcy lets you reorganize your debt and pay it off over time. Often, your payments are adjusted based on your ability to pay, which can reduce the total amount you owe. Federal law generally limits these repayment plans to three to five years in most consumer cases. See 11 U.S.C. § 1322(d) (2024).

Filing for bankruptcy can reduce the stress of constant calls from debt collectors. It can also stop late fees, and ease the pressure of not being able to make ends meet.

Related Guide: How Much Debt Do You Need to File Chapter 7 Bankruptcy?

2. Protection from Creditor Actions (Automatic Stay)

When you file for bankruptcy in Texas, an automatic stay is immediately put in place. This stops most collection actions, including wage garnishments, foreclosure, repossession, and creditor lawsuits, under the automatic stay in 11 U.S.C. § 362(a). However, there are exceptions in 11 U.S.C. § 362(b), such as certain family-law obligations and some repeat filings. The stay gives you breathing room by halting aggressive actions from creditors.

If you are behind on mortgage payments and facing foreclosure, filing Chapter 13 bankruptcy can stop the sale of your home. It gives you time to catch up. Chapter 13 lets you pay overdue mortgage amounts through a plan with manageable monthly payments.

This protection is one of bankruptcy’s most beneficial aspects. It provides temporary relief, allowing you to get back on your feet without fearing losing property or income.

Related Guide: Filing Chapter 7: What Happens to My Cosigner?

3. A Fresh Start and Financial Rebuilding

One of the greatest advantages of bankruptcy is the opportunity for a fresh start. Once your bankruptcy case is completed, you will no longer carry the burden of overwhelming debts. The liabilities that once felt insurmountable will no longer weigh you down. Bankruptcy gives you a chance to rebuild your financial life. It allows you to control your finances without the weight of past misfortunes.

After your debts are discharged or reorganized, you can begin rebuilding your credit. Your credit score may drop temporarily after you file for bankruptcy, but it can improve over time as you show responsible financial behavior. Many people start rebuilding their credit within a few years by paying bills on time, reducing debt, and managing credit wisely.

RELATED: 7 Reasons to File Bankruptcy in Texas

Cons of Filing for Bankruptcy

Although bankruptcy provides many benefits, it also comes with its own set of challenges and drawbacks. It’s important to understand these potential downsides before deciding whether bankruptcy is the right choice for you.

1. Impact on Your Credit Score

One of the most significant disadvantages of bankruptcy is its negative impact on your credit score. While bankruptcy provides debt relief, it will stay on your credit report for several years, making it more difficult to secure loans from lenders in the short term.

For a Chapter 7 bankruptcy, it will remain on your credit report for up to 10 years, consistent with the Fair Credit Reporting Act’s allowance for reporting bankruptcies. See 15 U.S.C. § 1681c(a)(1) (2024).

This can make qualifying for loans, credit cards, and mortgages more difficult in the short term. However, it’s important to keep in mind that rebuilding your credit after bankruptcy is possible. Many people find that they can improve their credit score over time by demonstrating good financial habits.

Additionally, bankruptcy will not affect all types of credit equally. For example, getting a secured credit card or car loan may still be possible after bankruptcy. However, these may come with higher interest rates.

2. Loss of Certain Assets (Chapter 7)

While Chapter 7 bankruptcy offers the benefit of debt discharge, there is a possibility that you could lose certain assets. In a Chapter 7 case, a bankruptcy trustee may sell non-exempt property to pay creditors. The good news is that Texas bankruptcy laws offer a variety of exemptions. They protect your property, such as certain personal property and retirement accounts, through homestead and personal property protections in the Texas Property Code. See Tex. Prop. Code §§ 41.001–.002, 42.001–.002 (West 2024).

However, if you have non-exempt assets, you may lose them during liquidation. For example, if you own valuable property that is not protected under Texas exemptions, the trustee may sell it to satisfy your debts. Chapter 13 bankruptcy, on the other hand, does not involve liquidation, but it requires you to pay off a portion of your debts through a plan approved by bankruptcy court.

The potential loss of property is a serious consideration for individuals who own valuable assets and want to protect them.

3. Bankruptcy Doesn’t Discharge All Debts

While bankruptcy can eliminate many types of debt, there are some debts that cannot be discharged through either Chapter 7 or Chapter 13. These debts include categories of nondischargeable obligations listed in 11 U.S.C. § 523(a). See 11 U.S.C. § 523(a) (2024):

- Federal student loans (except in rare cases of undue hardship)

- Child support and spousal maintenance (alimony)

- Tax debts owed to the IRS (with some exceptions)

- Criminal fines and restitution

- Debts incurred through fraud or misrepresentation

Additionally, while bankruptcy can help you reorganize your debt, it does not cut obligations like your mortgage or car loan. If you’re filing Chapter 13, you’ll still need to make regular payments on these secured debts. You will also need to adhere to the repayment plan, which can last several years.

Related Guides:

- Can Gambling Debt Be Discharged in Bankruptcy in Texas?

- Can Utility Bills Be Included in Chapter 7 Bankruptcy in Texas?

- Can Unemployment Overpayment Be Discharged in Chapter 7 Bankruptcy in Texas?

Key Considerations When Filing for Bankruptcy in Texas

| Pros | Cons |

|---|---|

| Debt discharge or reduction | Impact on your credit score |

| Protection from creditor actions | Loss of certain assets (Chapter 7) |

| Fresh start and financial rebuilding | Bankruptcy doesn’t discharge all debts (e.g., student loans, child support) |

Whether you file for bankruptcy or explore debt management options, it’s a serious decision, but with the right guidance, it can give you a fresh start. Don’t hesitate to reach out to Warren & Migliaccio, L.L.P. for legal advice tailored to your financial situation.

Case Study: Choosing the Right Chapter to Protect a Texas Home

A married couple—I’ll call them David and Maria—came to us scared they would lose their Dallas home. Credit cards, medical bills, and a repossession threat on their truck left them feeling embarrassed, overwhelmed, and out of options.

We started by walking through their income, debts, and exact home equity. Then I explained, in plain English, how Texas homestead exemptions work and the real-life pros and cons of Chapter 7 versus Chapter 13. Together, we confirmed their equity was fully protected and that a Chapter 7 case could clear their unsecured debt without risking the house.

After we filed, the automatic stay stopped collection calls and the trustee confirmed the home was exempt. Most of their unsecured debt was discharged. The takeaway: when you understand exemptions and choose the right chapter, bankruptcy can be a practical way to protect your home and reset your finances.

Frequently Asked Questions

Bankruptcy Basics in Texas

Will I lose my house or car if I file bankruptcy in Texas?

Most people keep their house or car in a Texas bankruptcy if they stay current on payments and their equity fits within Texas exemptions or a Chapter 13 plan. You may lose a property only if equity exceeds exemption limits or if you fall behind on secured loans.

- Texas homestead exemption protects your primary residence from most creditors, subject to exceptions such as purchase-money liens, property taxes, and other encumbrances listed in Tex. Prop. Code § 41.001(b)

- Vehicle exemptions protect equity up to statutory limits

- Staying current on payments is essential

What are the main pros and cons of filing bankruptcy in Texas?

Bankruptcy can eliminate many unsecured debts and immediately stop collection actions, giving Texans a financial reset and relief from overwhelming stress. Downsides include a damaged credit score, possible loss of non-exempt assets, and the fact that certain debts—like support and many taxes—cannot be discharged.

- Major pro: debt relief and automatic stay

- Major con: long-term credit impact

- Some debts survive bankruptcy

How long does a bankruptcy stay on my credit report in Texas?

A Chapter 7 bankruptcy generally stays on your credit report for up to ten years, while a completed Chapter 13 typically appears for seven. Many Texans start rebuilding credit within months by paying bills on time, keeping balances low, and using secured credit products responsibly.

Which is better for me in Texas: Chapter 7 or Chapter 13 bankruptcy?

Chapter 7 is usually faster and helps Texans erase large unsecured debts when income is limited and assets are modest. Chapter 13 works better when you need to catch up on a house or car or protect assets with significant equity. The right choice depends on income, property, and goals.

Collections, Exemptions, and Protected Property

Can filing bankruptcy in Texas stop foreclosure, repossession, or wage garnishment?

Yes. Bankruptcy triggers an automatic stay that stops most collection actions immediately, including foreclosure sales, repossessions, and wage garnishments. In Chapter 13, you can catch up missed mortgage or car payments. In Chapter 7, protection may be brief if you cannot stay current.

- Stops foreclosure during the stay

- Halts repossession attempts

- Freezes most lawsuits and garnishments

What debts cannot be wiped out if I file bankruptcy?

Bankruptcy removes many unsecured debts, but some obligations nearly always survive. These include most student loans, recent tax debts, child support, spousal maintenance, criminal fines, and debts involving fraud or intentional harm. Secured debts must be paid to keep collateral such as a home or vehicle.

How do Texas bankruptcy exemptions protect my home and property?

Texas exemptions protect essential assets so you can move forward after filing. The homestead exemption shields your primary residence, while personal property exemptions cover household goods, certain vehicles, tools of your trade, and most retirement accounts. Only non-exempt assets are at risk of sale.

- Unlimited homestead protection (subject to acreage limits)

- Strong personal property categories

- Broad retirement account protection

Alternatives, Costs, and Family Impact

Is it better to file bankruptcy or try debt consolidation or settlement first?

Bankruptcy is often best when debt is unmanageable and repayment within a few years is unrealistic. Consolidation or settlement may help if income is steady and the goal is lower payments, but they do not offer the automatic stay or the full legal relief bankruptcy provides.

How much does it cost to file personal bankruptcy in Texas?

Costs include federal court filing fees, required credit-counseling and debtor-education courses, and attorney’s fees. Chapter 13 cases typically involve higher total fees due to the length and complexity of repayment plans. Many firms offer payment options for Chapter 7 clients.

Will filing bankruptcy in Texas affect my spouse or community property?

Because Texas uses community-property rules, a bankruptcy filing can affect both spouses even if only one files. Most community assets that are under the filing spouse’s management and subject to creditor claims become part of the bankruptcy estate, but the non-filing spouse’s separate property is usually protected under Texas community-property rules and 11 U.S.C. § 541(a)(2). Joint debts may still appear on both credit reports.

Is Bankruptcy the Right Choice for You? Warren & Migliaccio can Help You Decide

Deciding whether to file for bankruptcy in Texas is a personal choice that should be based on your unique financial situation. For some people, Chapter 7 bankruptcy offers the cleanest path to a fresh start. Others may be better served by a Chapter 13 repayment plan, debt consolidation, or working with a credit counselor to regain control of their financial future. It’s important to weigh the pros and cons before making a decision.

If you’re considering bankruptcy or exploring credit counseling, working with a bankruptcy attorney can help you navigate the bankruptcy process. At Warren & Migliaccio, L.L.P., we have years of experience guiding individuals and families through Chapter 7 bankruptcy cases. We can help you understand the potential benefits and drawbacks of filing for bankruptcy in Texas and work with you to develop a strategy that aligns with your goals.

Whether it’s Chapter 7 or Chapter 13, we’ll help you understand your options and develop a plan that aligns with your financial goals. We are currently not taking new Chapter 13 cases, but can refer you to a trusted attorney if that is the best path for you.

Call our law firm at (888) 584-9614 or contact us online for a free consultation. Take the first step toward reclaiming control over your finances.

Disclaimer: This blog is for informational purposes only, consult the professional for legal advice.

Leave a Reply